Are distribution-connected batteries the best and fairest?

Are our electricity distribution grids the best and fairest place to host battery storage? It’s the only place where the value to customers of moving energy across time can be efficiently stacked to include the greatest energy market and network value. More importantly, batteries on the grid side of the meter can be used for the benefit of all customers, not just those who can afford to buy them, making grid batteries a fairer option.

The batteries are coming!

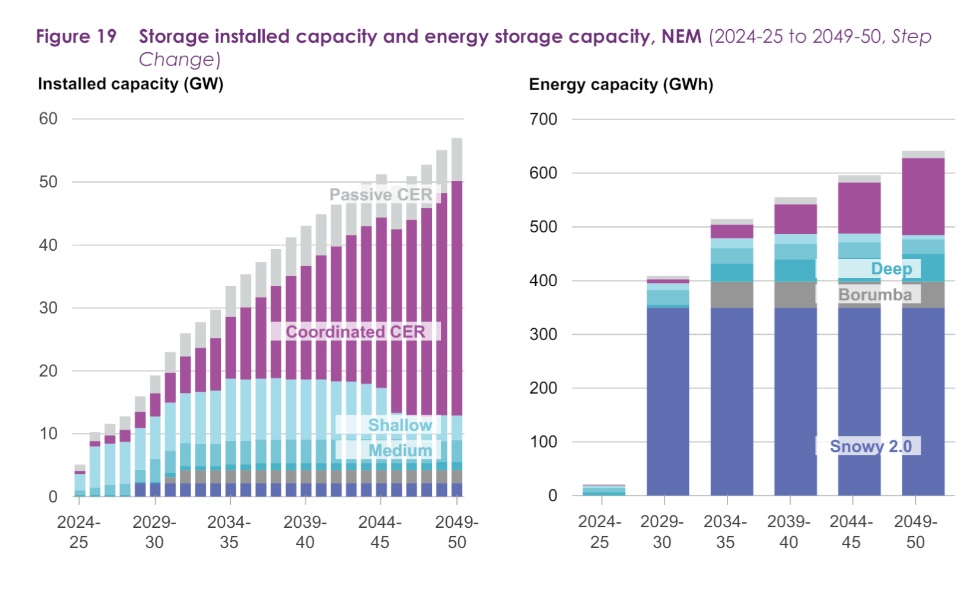

The 2024 draft integrated system plan, developed by the Australian Energy Market Operator (AEMO), highlights the enormous role that energy storage will play in the future grid. This includes customer energy resource (CER) batteries installed behind customer meters, as well as grid-scale storage and deeper energy storage systems such as pumped hydro.

Racking and stacking the value of batteries

We’ve previously noted the versatile roles that batteries can play as the Swiss-army knife of the grid. The balance between power capacity (in MW) and energy capacity (in MWh) varies across a broad spectrum and determines the role a storage system is best suited to playing, such as:

- Shorter duration resources – CER batteries or ‘two-hour’ grid-scale batteries – are suited to moving smaller volumes of energy around during the day. For example, from the middle of day (when solar is producing) to the evening (when we are heating and cooking in our homes). Filling small gaps.

- Longer duration resources –pumped hydro or other long duration technologies – are suited to moving much larger volumes of energy across weeks or months. For example, from windy and sunny weeks or months to be used during extended periods of lower wind and solar output.

These roles for storage create real value for customers. However, the focus is on the reliability of electricity supply. That is, ensuring the supply is there to balance with demand (usage) in real time in a system that is increasingly dominated by renewable sources of generation.

The reality is that electricity supply and demand are not connected by magic. They are connected by a vast physical network of poles, wires, transformers, switching stations and so on. This physical system is placed under new stresses and operating conditions due to the vast changes in the patterns of supply (increasingly weather dependent) and demand (increasingly flexible and, due to high penetration of rooftop solar photovoltaic (PV), also weather dependent).

Many of the challenges faced by the physical electricity system in the future grid can also be alleviated by moving energy across time. Batteries can provide network service value to the users of the shared electricity grid by:

- reducing the ‘peak’ electricity load – this can avoid the cost of investing in firming the physical grid assets to withstand higher electricity flows (e.g. substation upgrades).

- allowing more hosting capacity for residential solar PV – i.e. safely allowing more homes to export excess solar into the grid.

- reducing minimum net system load – excess solar during the day reduces system load and, if left unmanaged, will drive higher network costs in the future grid. Batteries that soak up this excess solar can help avoid these network costs

- helping control voltage – this can help networks keep the system within the technical limits at lowest cost to customers

- providing backup power – this can reduce the impact of a network constraint or outage, which is particularly useful for remote areas

- providing a more resilient grid – linked to the point above, in the face of natural disasters or other emergencies, battery storage can provide backup power to critical infrastructure, reducing outages and improving grid and community resilience beyond simple measures of electricity system reliability.

Batteries can also provide further value to the market and networks. For example, they can help control frequency on the power system by interacting with frequency control markets. They can also provide system security services, such as inertia and system strength, which transmission businesses are responsible for procuring.

Batteries in the future grid will likely be at all scales and locations. The tricky question for policy makers will be in how to incentivise the right mix and balance of resources to ensure efficient energy costs for customers over the long-term. This will require a good measure of system planning and, alongside it, some clear policy direction.

The case for distribution connected batteries (vs. CER)

The most important objective, as we move from around 5 GW of storage today to well over 50 GW in 2050, is to get the most out of these resources for customers. This means asking the critical questions; where should they go, and how are they best rolled out at scale (because there is no doubt they are needed at scale)?

There is a strong case for batteries to be hosted on the shared distribution networks (in front of the customer’s meter) as the most efficient and equitable approach to delivering battery storage at scale. This approach:

- is lower cost to deliver – a program of larger batteries (around 5 MW in capacity) can be rolled out at a lower capital cost per unit of installed capacity

- leverages the most network value – with batteries embedded in the right locations in the distribution grid, and operated appropriately, the network value noted above can be most effectively captured, and

- delivers certainty in operation – a smaller number of larger batteries on the distribution grid, with clear contractual arrangements to ensure operation that helps keep the grid within its limits, provides greater certainty of compliance and delivery of services to the network and market operator

Critically, this approach is also more equitable. CER batteries currently require government incentives to support uptake (e.g. $2,950 in Victoria and $2,400 in NSW), which in itself is a significant transfer of wealth to those who are able to afford the rest of the up-front cost of a battery. Battery owners will also be able to offset a larger proportion of their network and energy costs behind their meter, and, if orchestrated into a virtual power plant, will also be compensated for the value their asset provides to the broader energy system. Put simply; the ‘haves’ will capture the lion’s share of the value and the ‘have-nots’ will still be better off, but only marginally.

DNSP-owned, retailer-operated, medium-scale battery storage connected to the distribution grid could maintain the balance between a competitive market, ensuring system security and reliability, maximising the overlooked potential of the poles and wires in the street and help close the growing energy equity gap.

How can we best scale up distribution connected batteries?

The ability of batteries to provide both network services and market services means that both networks and other parties (most likely market facing parties) can lead the roll-out of infrastructure. There are, however, several natural advantages that a distribution network business might have in rolling out batteries at scale, allowing them to pass on a greater share of value to customers, including:

- the ability to move at speed and scale, fully leveraging scale efficiencies and delivering policy objectives on time (e.g. bringing down prices and emissions)

- the ability to use existing land assets (such as land adjacent to zone substations) to host batteries, lowering the cost of delivery. This also avoids the social license cost of procuring new land within communities and navigating its change of use

- the ability to fully embed battery storage into the planning and design of networks, for example, due to a network’s intimate knowledge of evolving demand and future infrastructure augmentation, replacement and operational needs

- leveraging existing processes and workforce for the operation and maintenance of assets, and

- the ability to partner with market facing third parties at scale, which can reduce the barriers for those parties to manage wholesale energy market risks through physical hedging. This would also improve retail competition

This does not all mean that distribution connected batteries should only be built by distribution networks. Indeed, all network connected batteries will have value, and networks will need to do more to provide transparent and up to date information on evolving network needs, and also to provide efficient avenues for battery proponents to provide non-network services and to connect to the power system.

A ‘fit for the future’ regulatory framework

It is critical that a distribution network roll-out of batteries transparently and effectively addresses the ‘who pays for what’ question. While customers ultimately pay, it is important that networks only recover the costs of batteries to the extent that they provide valuable network services to customers. Helpfully, there are existing regulatory tools to manage this, such as the cost allocation methodologies that each network business has approved by the Australian Energy Regulator (AER). These methodologies define the network’s approach to allocating costs between the different categories of services that it provides.

While networks can own batteries, they are restricted from using them for non-network services unless they obtain a waiver. This gives the AER comfort, on a case-by-case basis, that the arrangements in place for each network owned battery are appropriate. As all parties become comfortable with these bespoke arrangements, it is likely that in time they will prove unnecessary and can fall away in favour of more enabling and enduring arrangements for the transition.

Given the broad range of network services that batteries provide, it is likely that they will soon be seen as being as integral to the provision of network services as transformers or poles and wires. A direct analogy can be found in our gas transmission networks, which provide an inherent storage value (e.g. through line pack) that is valued by customers in their reliable gas supply.

It would be unusual if our battery ‘best and fairest’ award winner were to face pervasive or unnecessary regulatory hurdles to delivering core network services to customers as batteries shift from ‘innovative’ to ‘ordinary’. On the flip side, regulators will need to see real value for customers if they are to evolve their approach.

To help with this, ENA is currently partnering with L.E.K. Consulting and other modelling experts in a wide-ranging scenario modelling exercise designed to draw out the value of different actions that could be taken on the distribution grid to drive the greatest value for customers while helping deliver the transition. Our work will include looking into the value of distribution connected batteries in more detail. We will have more to say on this and other topics as this work tests and challenges our views on the most efficient path to decarbonise the energy system.