Are we up the GSOO without renewable gas?

In March each year, AEMO publishes its yearly Gas Statement of Opportunities report (GSOO). The media response is one of doom and gloom highlighting how Australia will run out of gas. But the real story is much more nuanced than that.

Headline findings of 2024 GSOO

The doom and gloom response is not surprising when one of the opening lines of the 2024 GSOO is:

The 2024 GSOO continues to forecast risks of shortfalls on extreme peak demand days from 2025 and the potential for small seasonal supply gaps from 2026, predominantly in southern Australia, ahead of annual supply gaps that will require new sources of supply from 2028. (2024 GSOO, pg 4) (emphasis added).

This clearly demonstrates projected gas supply shortages in the next 18 months and growing towards the end of the decade. This accounts for decline in gas consumption but a greater decline in gas supply:

Gas consumption by residential, commercial and industrial consumers is forecast to decline, but production in the south is forecast to decline faster. (2024 GSOO, pg 4)

Although these shortages are forecast to be short-lived and relate to peak winter days, they do reflect potential times when the gas demand exceeds the gas supply. This gas demand combines demand for industry, commercial and residential buildings as well as gas power generation.

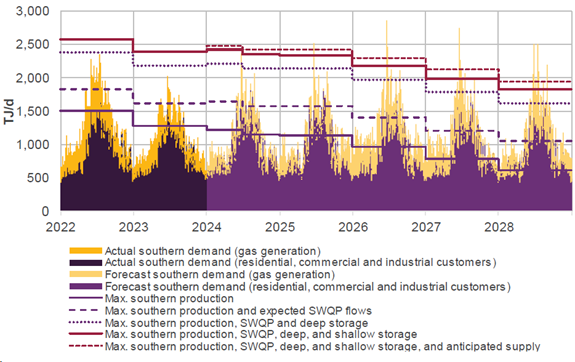

Figure 1: Daily southern gas system adequacy (Source: AEMO GSOO 2024, Figure 4)

Addressing short term supply

Figure 1 illustrates that there has been an imbalance between southern production and demand for the last few years, especially during the southern winter peak when gas is used for heating homes directly and also for supporting the electricity grid through gas fired power generation. Additional measures such as flow from Queensland and deep storage have been necessary to meet the gas demand. Ensuring sufficient gas supply for 2024 will require shallow storage as well as deep storage, and need to draw on infrastructure that is already in place or nearing completion (e.g. the East Coast Grid Expansion project[1]).

Addressing short term supply is best met through demand flexibility given the lead time needed to plan, obtain approval for, and build new greenfield infrastructure. AEMO notes that:

In extreme gas shortfall conditions, secondary fuels may be needed to operate gas generation for short periods so electricity reliability is not compromised. (GSOO 2024, pg 11)

In the longer term, southern gas supplies are declining and meeting the declining demand will require new gas supplies.

Declining demand

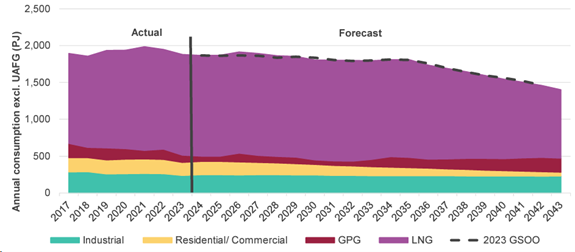

AEMO is also forecasting the domestic demand to decline out to 2043. Applying the scenarios from the Integrated System Plan[2] result in changing demand profiles.

Figure 2: Eastern coast gas demand to 2043 (Source: AEMO, 2024 GSOO, Figure 9)

A common feature from east coast gas is that around two thirds of the gas is exported. The LNG figures are based on forecasts from LNG producers out to 2035. Beyond this, AEMO has adopted trends in line with those observed in the International Energy Agency (IEA) forecasts[3]. The forecasts from 2035 apply increasing decarbonisation actions globally so reduce the levels of LNG exports as many countries seek alternative energy forms with lower emissions.

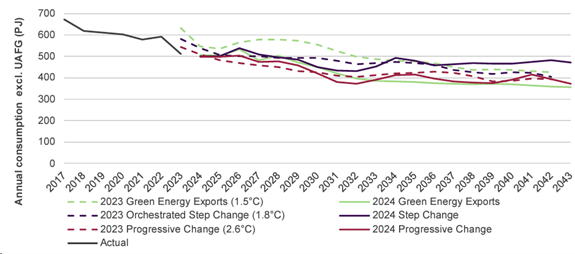

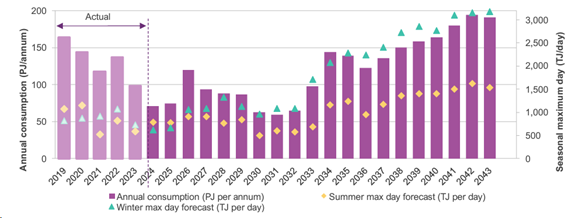

Domestic gas use is dominated by industrial users, businesses and homeowners for heating and the electricity sector for gas fired power generation.

Figure 3: East coast domestic gas use forecast by scenario (Source: AEMO 2024 GSOO, Figure 11)

The industrial demand remains fairly unchanged over the forecast period declining from a 2024 level of 245 PJ to around 230 PJ by 2043. One of the scenarios indicates a higher decline in gas consumption in industry driven by potential closure risks of some industries. Even in this case, gas demand in 2043 is projected to be around 175 PJ. The industrial sector provides a bedrock for gas demand on the east coast. And an opportunity for renewable gas deployment.

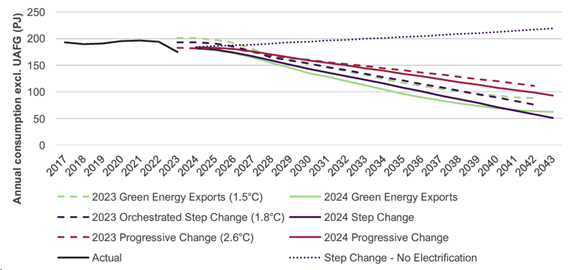

Within AEMO’s modelling, electrification is the main mechanism to reduce gas demand. Between 140 and 200 PJ of gas demand is electrified over the period to 2043 in the model. Most of this is projected to occur in the residential and commercial sectors following the introduction of policies to limit future gas connections in Victoria and the ACT. Nonetheless, AEMO notes that there is high uncertainty around this:

The pace of investments to electrify remains a key uncertainty in AEMO forecasts (GSOO, 2024, pg 23)

The assumptions made in the AEMO modelling would indicate that gas consumption in the residential and commercial sectors would decline to around 50 PJ by 2043, from a 2024 total of 175 PJ. This also implies a reduction in residential gas connections from 5 million on 2024 to less than 2 million in 2043.

Achieving this level of consumer behaviour will require a strong set of policies and messaging and AEMO recognises this as a key uncertainty in their modelling. Hence, they included a consumption forecast in the absence of policy driven electrification, which shows an increase in natural gas consumption for the residential and commercial sectors. The future is hard to predict. While some customers may choose to electrify, others may choose to remain on gas and to convert to renewable gas over time.

Figure 4: Residential and commercial sectors gas forecast (Source: AEMO, GSOO 2024, Figure 15)

It should be noted that forecasts are useful tools to better understand what the future could be, not predictions of what it will be.

Gas is also a key fuel for supporting the electricity grid. While annual gas consumption for power generation has decreased in the last couple of years, it is forecast that this will increase again towards the end of the decade as more coal fired power stations are decommissioned and gas generation is called on more often to support variable renewable generation (alongside batteries, hydro and demand management).

Figure 5: Gas demand for power generation (Source: AEMO GSOO 2024, Figure 21)

Reduced gas demand for winter heating from electrification of the residential sector drives increased winter gas demand for power generation.

Addressing long term supply and renewable gas supply opportunities

Combining the individual sectors indicates that natural gas demand is declining. But the GSOO notes that supply is declining faster, resulting in a supply adequacy gas by the late 2020s.

New fields, improved storage, new pipeline connections and LNG import facilities all provide additional supply opportunities.

Renewable gas, such as biomethane, or hydrogen produced via electrolysis using renewable energy resources, also provide new supply for gas. The 2024 GSOO includes current and future supply from a small number of existing or committed renewable gas projects[4]. There are many proposed but uncertain renewable gas supply projects that are subject to a range of economic, regulatory and technical uncertainties. This makes the timing and volumes of gas available from renewable sources is therefore challenging to forecast. Nevertheless, AEMO estimates annual volumes of renewable gas may be up to 30 PJ/y by 2031, depending on the timing of these development opportunities. The potential or renewable gas beyond 2031 will depend on ongoing technology developments and supportive policy settings.

Closing the gas supply gap

The GSOO identifies near term and medium term gas supply gaps reflecting a decline in east coast gas demand and a greater decline in supply. The near term supply gaps can be managed from redirecting gas to the southern markets and completing current projects to provide more supply. Longer term projects will need more greenfield infrastructure and new gas supply source. Renewable gas can help meet this supply but supportive policy settings (such as certification) will be needed to scale up the renewable gas market.

[1] https://company-announcements.afr.com/asx/apa/43ea1679-dbb0-11ec-a040-c29688956f17.pdf

[2] https://aemo.com.au/en/energy-systems/electricity/national-electricity-market-nem/nem-forecasting-and-planning/integrated-system-plan-isp

[3] https://www.iea.org/reports/world-energy-outlook-2023

[4] For example, Australian Gas Networks Hydrogen Park – SA project or Jemena’s Malabar Biomethane Injection Plant.