Networking opportunities: future-proofing the National Gas Rules

The total pipeline length of Australia’s gas distribution networks would stretch around the earth’s equator twice, and represents a significant national energy asset. For example, Australia’s gas infrastructure can store the same amount of energy as six billion Powerwalls. Whether it is for hot water, heating, or cooking, gas plays a central role in the lives of over 6.5 million Australian households.

The scope of economic regulation for the pipelines used to provide customers with gas is the subject of a current Australian Energy Market Commission (AEMC) review. It poses important questions around how gas transmission pipelines and networks are regulated. Amidst a significant focus on electricity prices, and rising wholesale gas costs across eastern Australia, the review provides a unique opportunity to reflect on the performance of a broader gas regime introduced a decade ago.

A significant focus for the review is taking forward recommendations concentrating on the scope of transmission pipeline regulation, regulatory controls applying to pipeline expansions and information and dispute resolution. For gas distribution networks, which are mostly subject to economic regulation through the intensive ‘full regulation’ model under the National Gas Law and Rules, these are less central issues.

For gas networks, there are critical strengths to recognise in the existing regime. These include:

- well-defined circumstances of regulatory discretion which provide transparency and reduce the potential for disputes;

- a spectrum of lighter handed regulatory and other oversight options, which is appropriate given the range of different market circumstances from large urban gas networks and smaller regional networks featuring strong inter-fuel competition; and

- flexibility, ensuring the regime can be responsive to changing customer needs and innovation.

These strengths have supported the strong overall performance of the gas regulatory regime for customers – and they can be built on in the current review.

Stable or falling network charges

In a challenging environment for gas wholesale charges, the existing National Gas Rules have delivered stable or falling network revenues and prices in a way that has reflected ongoing increases in efficiency and changes in input costs.

As an example, the Australian Energy Regulator (AER) has estimated that in the current round of AER decisions, allowed network revenues are forecast to fall by an average of 12 per cent, compared with the previous round of decisions.[1] This is reflected in an average annual reduction of over two per cent per annum for the current round of AER gas network determinations.[2] Falling input costs and continued efficiency enhancements are delivering material relief for gas customers experiencing higher gas wholesale gas prices. As an example, the largest overall fall in energy distribution charges is expected for Jemena gas networks serving New South Wales, with forecast reductions in network costs expected to deliver savings to residential customers’ bills of almost 25 per cent.[3]

Growing customer connections

Over the past fifteen years the gas regime has supported the expansion of access to natural gas from approximately 3.4 million to around 4.5 million residential households.[4] This is reflected in the growth of gas distribution networks from 75,500 to 88,636 kilometres in the same period.

The substantial growth in customer numbers and connections over the past fifteen years benefits existing customers by spreading the largely fixed costs of network service provision over a broader customer base. This allows customer prices to be lower than otherwise would be the case. Expansion of gas availability to new households and commercial users provides further competitive pressure on other fuel sources, such as electricity, wood, and LPG, as well as the direct customer benefits of the flexibility of new gas service offerings.

Customer satisfaction

The recent Energy Consumers Australia Energy Consumer Sentiment Survey released in June 2017 outlined a series of survey findings around gas consumers’ experience under the existing overall gas regulatory regime.

It is important to note that the survey delivered single responses on consumers’ overall experience with an energy source, and not on their experience or assessment of the different potential contributions made by wholesale, retail and network components of the services. Nonetheless, the survey provides the only standardised national assessment of ordinary household and small business consumer views on the performance of gas services.

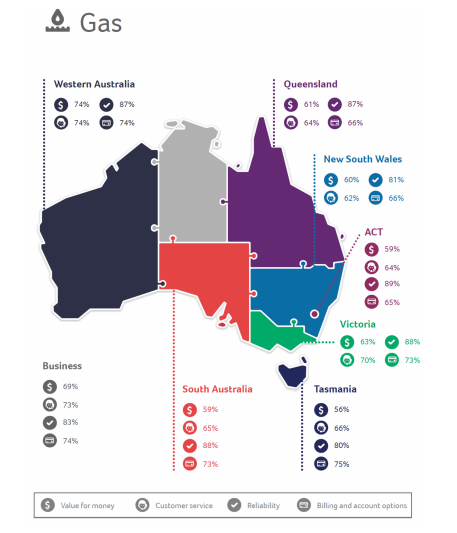

Satisfaction with overall value for money is up in all markets, except for South Australia.[5] Around 69% of small business customers are satisfied with their value for money, up 10 per cent over the last year.[6] When compared by those customers to other utilities such as electricity, internet service providers, water, insurance and banking, gas is rated as the best value for money utility service. Gas customers across Australia uniformly report high levels of satisfaction with reliability, of between 80-88 per cent. Due to the specific technical characteristics of gas network operations, planned and unplanned service interruptions are extremely rare and typically occur due to third party damage to gas infrastructure, rather than network asset failure. It has been estimated that a typical residential gas customer, under current levels of reliability, could be expected to experience an outage approximately every 40 years.

Source: Energy Consumer Sentiment Survey – Key findings for households, June 2017 (page 8).

‘Future proofing’ gas network rules

The flexible and non-prescriptive nature of the existing National Gas Rules is a source of strength of the regime, and enhances its capacity to develop through time and be responsive to changing customer needs. This has facilitated gas network businesses, and the AER, experimenting successfully with new models and forms of extended customer engagement, delivering more customer focused regulatory outcomes than previously.

One area that may require further policy focus from rule-makers and governments, however, is ensuring unintentional roadblocks to the creative future use of gas networks are removed.

An example of this is the current definition of gas under the regulatory regime referencing methane. Australian gas distribution networks are increasingly looking to explore the potential to use non-methane based fuels in existing natural gas distribution systems.

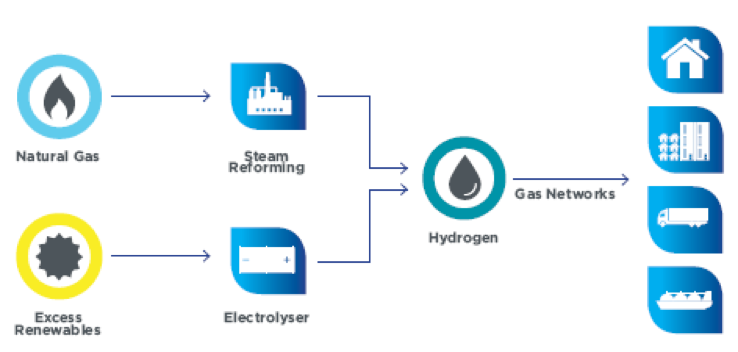

An Australian first “power-to-gas” trial announced this month could see excess renewable energy stored in the gas grid and used to decarbonise Australia’s gas supply. Australian Gas Networks will partner with AquaHydrex, which will design and build an electrolyser pilot plant in Adelaide’s western suburbs. It will use electricity to split water to produce hydrogen – a carbon-free fuel – which will then be blended with natural gas and injected into South Australia’s gas grid. This stored energy can then be used when it’s needed to stabilise intermittent solar and wind power.

Source: Gas Vision 2050

This is just one example of Australian gas innovation as the industry embarks on its decarbonisation journey. We should be ensuring regulatory arrangements can support such innovation, while building on the existing strengths of this flexible regime which have already served Australian customers so well.

[1] AER State of the Energy Market, May 2017,p.107

[2] See Figure 3.7, AER (May 2017), p.109

[3] AER (May 2017), p.109

[4] Productivity Commission Review of the gas access regime – final report, 2004, p.12

[5] Essential Research- Energy Consumers Australia Energy Consumer Sentiment Survey June 2017, p.16

[6] Essential Research (June 2017), p.35