Toward the long term integration of carbon and energy policy

The outcome of COP 21 in Paris last December provided a welcome commitment from 195 countries to address climate change. With other nations, Australia committed to limiting climate change to 2 degrees Celsius, and embraced the target of a 1.5 degree limit.

Australia’s carbon policy is approaching a crossroads. The next Federal Government will determine not only what targets are set for 2030 and beyond, but how efficiently we meet our carbon abatement objectives. A re-elected Coalition Government would need to substantively overhaul the Safeguards Mechanism for the Emissions Reduction Fund to achieve a reduction of 26-28% below 2005 levels by 2030. The ALP has announced an initial target of 45% below 2005 levels by 2030, with a final target to be soon determined after recent consultation with industry.

There is a stated commitment by energy ministers, through the COAG Energy Council, for a national cooperative effort to better integrate energy and climate policy, with a clear focus on ensuring that consumers and industry have access to low-cost, reliable energy as Australia moves towards a lower-emissions economy[1]. This must include shaping long term carbon policy to deliver the best outcomes for customers in the period to 2030 and beyond.

The Energy Networks Association (ENA) engaged Jacobs to undertake an analysis of carbon abatement policy options and the outcomes for consumers, with a view to informing decisions on long term carbon and energy policy settings.

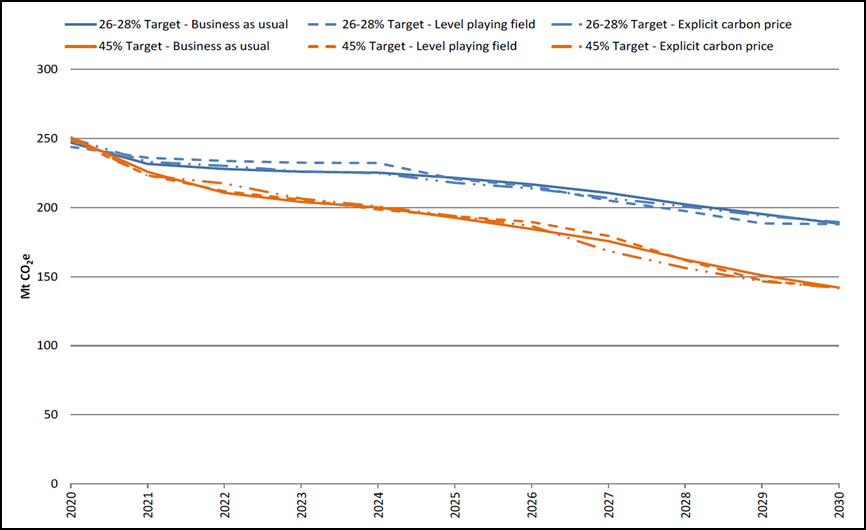

The preliminary findings of the modelling, presented last week by the ENA at Australian Domestic Gas Outlook 2016, compared a Business as Usual scenario with a Level Playing Field scenario and an Explicit Carbon Price scenario (see Figure 1 below). The analysis considered the performance of different policy scenarios in achieving two abatement targets – the current Australian Government target of a 26% to 28% reduction by 2030 and the Opposition target of a 45% reduction by 2030.

Figure 1: Overview of Policy Scenarios analysed

| Scenario | Key Features |

| Business As Usual | Assumes the continuation of the diverse range of various State and Federal abatement initiatives which prescribe specific technologies (e.g. renewables) or scale (e.g. SRES, FiT) and the extended use of a binding Safeguards Mechanism which limits sectoral emissions without trading. In addition, in the 45% target scenario a carbon price and 50% RET is assumed. |

| Level Playing Field | Assumes the current abatement initiatives are made technology neutral (e.g. via a low emissions target scheme) and indifferent to scale. In the 26-28% target, it assumes that the Safeguards Mechanism evolves to a baseline & credit mechanism permitting trading among generators. In addition, in the 45% target scenario a carbon price and 50% LET is assumed. |

| Explicit Carbon Price (only) | This scenario assumes that an explicit carbon price is established through a mechanism equivalent to a whole of economy carbon tax or emissions trading scheme. All other abatement policies (e.g. RET, SRES) are removed. |

The Jacobs analysis confirms that the economy-wide carbon reduction targets could be achieved in the stationary energy sector by 2030 using all of the different policy approaches.

Figure 2: Abatement trajectories by Policy Scenario

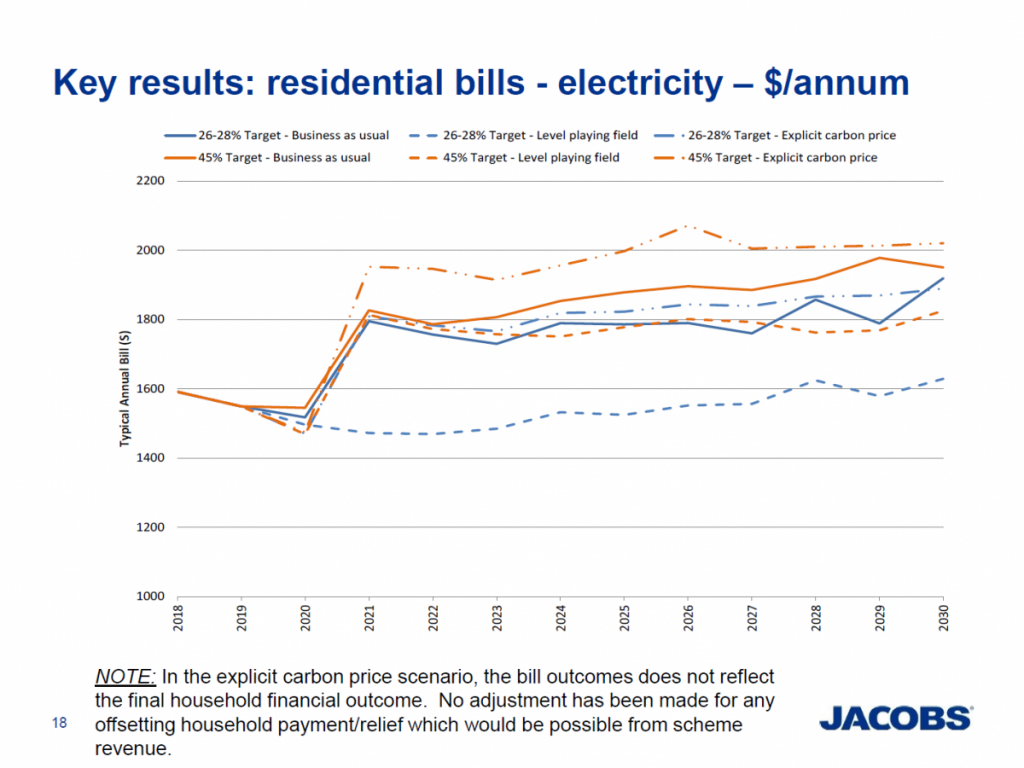

These initial findings indicate that the lowest residential bills occur under the Level Paying Field scenario, where abatement policies are ‘technology neutral’. A typical residential customer would save an average of $234 per year on their electricity bill between 2020 and 2030 (see Figure 3) and Australia would still meet its emissions reduction targets. The cumulative saving over the decade would represent approximately $2500.

Figure 3: Outcomes for residential electricity bills to 2030

Under the technology neutral, Level Playing Field scenario, the Renewable Energy Target (RET) is expanded to become a Low Emissions Target (LET), which supports emissions abatement from not only renewables, but other low emissions generation.

Technology neutral policies will still see significant growth in renewable energy, but achieve abatement targets at lower cost. The preliminary results of the Jacobs modelling indicate that renewable energy output will continue to grow over the period modelled between 45% and 202% depending on the scenario.

Under the ‘technology neutral’ scenario, the Emissions Reduction Fund’s Safeguards Mechanism would become a ‘baseline and credit’ scheme, which permits emissions trading within the energy sector. A baseline of emissions intensity (tonnes of CO2 per MWh sent out) is set for the electricity sector and then reduces from 2020 to 2030 to meet the emissions target. Generators with emissions intensity above the baseline can trade with generators with emissions intensities below the baseline to cover their emissions liabilities.

The modelling shows the opportunity for consumers to save money if carbon policy focusses on the outcome – lower emissions – such that all technologies compete based on their ability to efficiently achieve abatement. Indeed, Jacobs preliminary findings suggest that savings from technology neutral policy settings could be enough to offset an increase in the abatement target from 26-28% below 2005 levels by 2030, to 45%.

The Jacobs analysis also indicates an explicit carbon price delivered the lowest cost to the Australian economy, with savings of up to $8.2 billion under a 45% target, when compared to current policy settings. However, in this scenario residential electricity bills were higher and the household financial outcome would depend on how any offsetting payments were made from scheme revenue.

Australia can achieve its current and future carbon targets efficiently and minimise the impacts on electricity customers, but it requires a level playing field from government policy, and market-based mechanisms that are broadly applied across the energy sector.

Further information on the preliminary results is available here, with the Final Report to be released in coming months.