Regulating gas in a transforming energy system

The economic regulatory framework for gas distribution networks was developed when gas was Australia’s fastest growing fuel, with growth expected to be sustained into the future. However, our decarbonising economy means moving to renewable gas or electrification of gas services, which will decrease gas demand. This poses challenges to the framework.

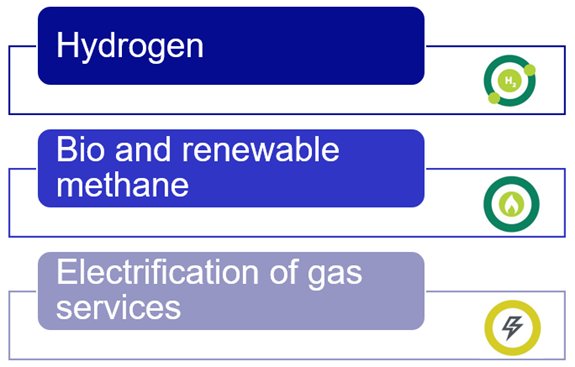

Gas is changing. Australia’s gas networks have been at the forefront of that through Gas Vision 2050, which advocates replacing natural gas in networks with hydrogen, biomethane or a blend of both. There are also policy drivers that promote electrification, which may be a suitable option in some cases.

Figure 1: Technology pathways for replacing natural gas in networks (Source: Energy Networks Australia)

As a result, the demand for natural gas is likely to decline in the longer term. Replacing this with hydrogen or biomethane will be subject to technical regulation to ensure ongoing safe operation of the network. However, this will also impact on economic regulation, which currently only covers natural gas[i]. The Australian Energy Regulator (AER)[ii] published an information paper recently that lays out different regulatory options and tools that might protect the long-term interests of energy customers in a time of uncertainty.

Economic regulation is applied to gas distribution networks to set tariffs for delivery of natural gas. This framework aims to stop networks exercising monopoly power and was developed at a time when gas markets were growing. It did not contemplate a decline in natural gas. As the AER notes:

The national gas regime was developed at a time when the gas market was growing and was expected to continue to expand. The regulatory framework is predicated on the assumption that natural gas service providers can exercise monopoly power if unregulated. The regulatory framework does not appear to contemplate a scenario of curtailment or decline in natural gas demand, or that gas networks may have an end-life. The market has evolved in ways unforeseen when the rules were developed. [AER, pg 59, emphasis added]

The AER identifies a range of drivers that contribute to uncertainty in natural gas demand:

- Decarbonisation policies adopted by current and future governments,

- Increasing competitiveness of renewable electricity (e.g. reduction in capital cost of rooftop solar PV),

- Energy efficiency improvements resulting in lower gas consumption,

- Uncertainty in future gas prices,

- Consumer sentiment towards gas,

- Corporate and investor activism, and

- Demand for gas to generate electricity.

The interaction and overall impact of these drivers is complex, contentious and uncertain. A broader discussion should be held to accurately identify the issues that impact the demand for natural gas and where alternative renewable gases provide strong commercial opportunities. For example, the fact that rooftop solar PV is becoming cheaper has a limited impact on gas demand because gas, especially for space heating, is used at a different time of the day and year compared with when rooftop solar is most productive. Similarly, one of the drivers notes a projected decline for gas to generate electricity but this does not reflect that gas is likely to become a more important and more frequently used source to complement variable renewable generation.

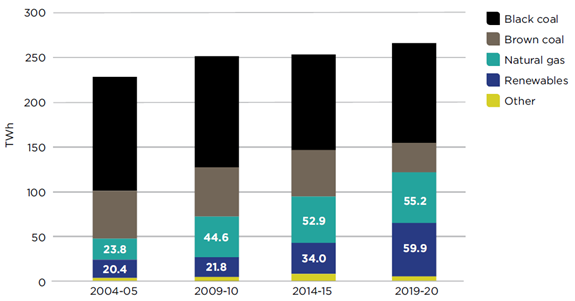

Figure 2: Gas fired generation supporting renewable generation across Australia (Source: Energy Networks Australia (2021), Reliable and clean gas for Australian homes).

While the impact of these drivers is unclear, the AER correctly identifies this uncertainty and is concerned about how this may impact gas access prices, as well as intergenerational equity between current and future customers.

We are concerned about how these uncertainties affect the way we determine efficient access prices over time and the intergenerational equity between current and future gas customers. There is the potential for an increase in gas access prices if gas demand drops sharply in the future, which will ultimately be borne by households and industry. (AER, pg 1)

There are four potential areas of impact from declining demand:

- A decline in gas connections results in fewer customers to share fixed costs of gas networks and may lead to increased prices.

- The cost burden of unpaid past investments may be shifted to future gas customers.

- The potential for the economic stranding of gas networks.

- The price volatility and uncertainty could further reduce demand resulting in further unequitable distribution of the cost burden.

The uncertainty is more complicated as the role of renewable gases can create a further opportunity to utilise gas networks.

In the longer term, the case for repurposing networks depends on the price of hydrogen compared with substitutes such as renewable energy. (AER, pg 14)

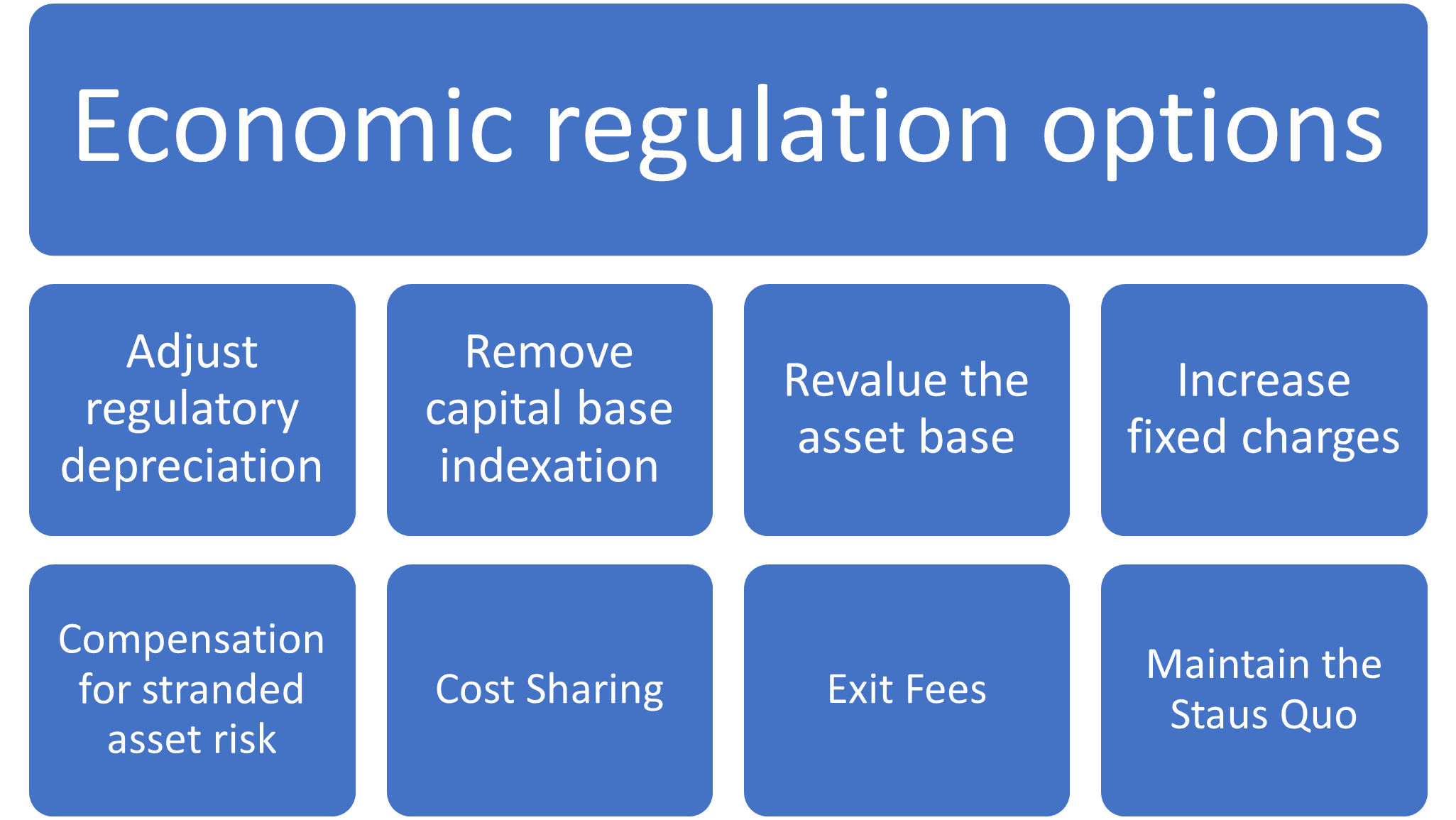

The AER has identified eight potential options to address this uncertainty and outlines a range of pros and cons for each. In essence, these options are all different forms of bringing forward the recovery of costs or recognising these greater risks in future decisions.

At this early stage of development, the AER is favouring the option to adjust regulatory depreciation, although it also notes that the options are not mutually exclusive. Accelerating depreciation for some assets allows the capital cost base to be recovered over a reduced period. The AER views this as the most appropriate option as it allows tariffs to be adjusted over time to facilitate an equitable and efficient allocation of costs between current and future customers. A benefit of this option is that it does not lock in a price change permanently and provides the greatest flexibility if the changes in demand turn out different than expected, or the network can be safely repurposed to carry renewable gases.

The other options outlined by the AER are:

- Compensation for stranded asset risk,

- Removal capital base indexation,

- Sharing costs under capital redundancy options,

- Revaluation of asset base,

- Introducing exit fees, or

- Increasing fixed charges.

Figure 3: Options to address uncertainty of gas demand (Source: ENA Analysis).

An option of “maintaining the status quo” is also considered. If the risk of asset stranding is not demonstrated to be material, it may not necessitate any regulatory action. Further, if a proposed action to address stranded asset risk is contrary to consumers’ long-term interests, the AER may not accept it either, resulting in the status quo.

Where to next?

Gas networks are changing, and different networks face different evolving market conditions. Yet in line with Australia’s climate targets, the gas delivered by 2050 will either be replaced by renewable gas sources or will be electrified. The AER has set out a framework and options that can be usefully explored in conversations with Australian energy consumers, investors and governments about how to protect the interests of current and future customers of the gas network.

[i] The AEMC and AEMO are currently consulting on extending the definition of natural gas to also cover other gases that can then subsequently be covered by economic regulation.

[ii] Australian Energy Regulator (2021), Regulating gas pipelines under uncertainty – Information paper, https://www.aer.gov.au/networks-pipelines/performance-reporting/regulating-gas-pipelines-under-uncertainty-information-paper