London Calling: Networks and the Transition

ENA recently had the opportunity to learn more about the energy landscape in the UK and the innovative projects, and frameworks, that are supporting the transition. We share some of the insights from the UK’s Energy Innovation Summit and further engagement with key players.

After wrapping my head around the tube again (trying to look like a local and failing), the weather (sorry Brits, this is one area where we are superior) and the UK-based energy acronyms, it was great to be back in the UK after a long stretch away.

What struck me most from the trip was the similarities we all share, even if at different starting points and perspectives, and how much we can learn from each other through further collaboration.

Maximising the potential of the distribution network

As we move away from a world with large, centralised power generation to one with lots of decentralised customer energy resources (CER) connected to our electricity grid, the role of the distributor is changing – no matter what the country.

Traditionally known as distribution network service providers (DNSPs) in Australia, or distribution network operators (DNOs) in the UK (following energy’s general-held view that more acronyms are better than fewer), we are increasingly seeing a transition to distribution system operators (DSOs).

DSOs, at a high-level, operate a more dynamic electricity network due to all the CER connected to the grid, and seek to optimally manage this CER to unlock customer value and reduce network investment, which then benefits all customers through lower bills.

We have explored this previously in the Australian context here, and UK Power Networks recently launched its own independent DSO to keep pace with the evolution of the electricity network, committing to delivering £410 million of savings over the next 5 years compared to a conventional approach to reinforcing (‘building out’) the network.

Figure 1: UK Power Networks – DSO

Source: UK Power Networks, DSO Forward Plan 2023/2024

The establishment of the DSO in the UK is also supported by clear incentives from Ofgem, the UK energy regulator.

Recognising that changes are needed to the operation of electricity distribution networks, in the most recent ‘price control’ (akin to our 5-yearly regulatory resets), Ofgem introduced DSO specific incentives. These new financial incentives will drive distributors to more efficiently develop and use their network, taking into account flexible alternatives to network reinforcement.

When considering the development of DSOs in Australia, there is likely value in – as Ofgem in the UK highlights – allowing distributors to tailor their approach to reflect their own circumstances and transition issues. There is probably no exact ‘one size fits all’ approach to implementation.

A common thread in discussions with UK market participants is that – just as in Australia – it is now more important than ever that we maximise the potential of the distribution networks in the energy transition.

Net zero needs a ‘Whole-of-Systems’ approach

After attending the Energy Innovation Summit, it is clear that ’whole-of-systems’ thinking is needed to get to net zero.

We learnt more about projects such as National Gas’ Project Union, the UK’s ‘hydrogen backbone’ that is aiming to join together industrial clusters around the country. Scottish and Southern Electricity Networks presented on its NeRDA (Near Real-time Data Access) Project, which is making near-real time data available to their stakeholders and interested parties via an online portal.

We also heard about Electricity North West’s Project QUEST, a whole-system voltage optimisation system that will cater for increased uptake and use of low carbon technologies.

The UK’s Electricity System Operator, soon to be the Future System Operator, is also running the CrowdFlex Project, which is exploring how domestic flexibility can be used to help manage the grid to deliver benefits to both consumers directly and the overall efficiency and resilience of the electricity network.

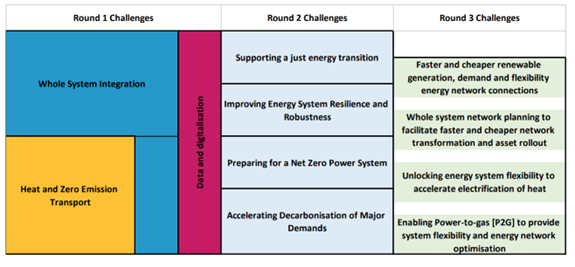

What is common in helping drive innovative energy network projects in the UK, however, is the active role of the regulatory environment in supporting these. For example, Ofgem has both a Network Innovation Allowance, and a Strategic Innovation Fund, or a ‘SIF’ for short, which is designed to fund the ambitious, innovative projects that are needed to transform electricity and gas networks.

Under the SIF, Ofgem sets the Innovation Challenges for the market to respond to (as shown in Figure 2 below) and, since launching in 2021, the fund is expected to invest £450 million by 2026, with the option to increase and extend as necessary. SIF is a funding mechanism within the current regulatory resets (or the ‘RIIO 2 price controls’ in UK terminology) and is open to both gas and electricity networks, along with the Electricity System Operator.

Figure 2: Ofgem’s Strategic Innovation Fund: Innovation Challenges

Source: Ofgem, Ofgem Strategic Innovation Fund: Round 3 Innovation Challenges – Final Decision, Figure 1

Supporting transmission investment

The UK, in its approach to regulating energy networks, has recognised the crucial role that major transmission projects play in meeting Government’s net zero targets, and the regulatory changes that have been made recognise that we are no longer in a steady state environment.

The implementation of Ofgem’s Accelerated Strategic Transmission Investment supports the accelerated delivery of the transmission projects that are needed to meet the Government’s renewable energy targets. It streamlines the regulatory approval and funding process to accelerate the delivery of these projects, recognising that there is a cost to delays. Ofgem’s Future Systems and Network Regulation work stream is considering how this needs to be further refined as the transition continues at pace.

Ofgem has also recently announced a new policy to clear ‘zombie projects’ from a lengthening connection queue and cut the waiting time for energy grid connection; shifting away the existing ‘first-come, first-served’ system, and allowing the fast track of ready-to-go generation and storage to enable net zero.

This is just a small taster of some of the insights we gleaned. I’d often come out of presentations and discussions with more questions than when I started, but what was clear to me is that there is strong alignment on where Australia wants to be, and lots of lessons to be learnt from each other on how we can get there. Just like navigating the tube, it can help to keep in mind that we all share a common set of destinations, and while each of our journey differs, we recognise that we are all working towards the transition together.