Cracked Rear View: What did the ACCC actually report on network prices?

For the period from 10 years ago to 2 years ago, the ACCC found increases in power bills were driven by higher network costs, increasing retailer costs and green scheme costs. But this is like driving forward while looking in the rear vision mirror. What’s happening now and what’s ahead of us?

The mixed picture of energy charges

This week the ACCC released its initial findings for the Australian Government commissioned inquiry into the retail supply of electricity and the competitiveness of retail electricity markets in the National Electricity Market. The Inquiry reviews the current state of Australia’s retail markets, and identifies some of the causes for recent price increases for consumers.

Beneath the headlines, one of the most useful aspects of the ACCC report is that it shows how the moving parts of the energy delivery chain go to make up a final electricity price, using 10 different sources of information which reference price trends and report on drivers of these trends.

The picture they paint is not as simple as all elements of the delivery of energy going up.

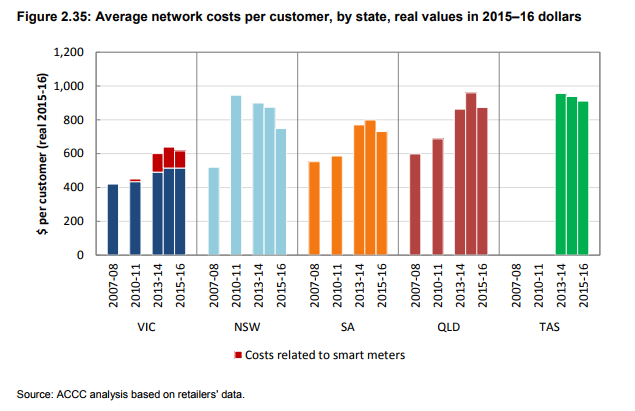

For example, ACCC analysis shows that across the five National Electricity Market States total network costs are now falling.[1] In turn, Australian Energy Regulator (AER) benchmarking data from network businesses shows falling revenue in every jurisdiction reviewed.[2]

This network costs trend is a result of significant reform elements still in the process of implementation, including movement to trailing financing cost approaches that smooth customer prices to reflect yearly cost changes. State governments have also recalibrated past prescriptive reliability standards that embedded significant costs, allowing less capital to be spent to deliver reliable supply. As the ACCC notes, new incentive schemes, such as those currently under development like the demand management incentive scheme also hold the promise of potential further savings. .[3]

The level of network contribution to rising retail prices has varied between jurisdictions and specific drivers in those jurisdictions. In South Australia, for example, the ACCC found that the regulated asset bases of the networks had increased only marginally over the last decade.

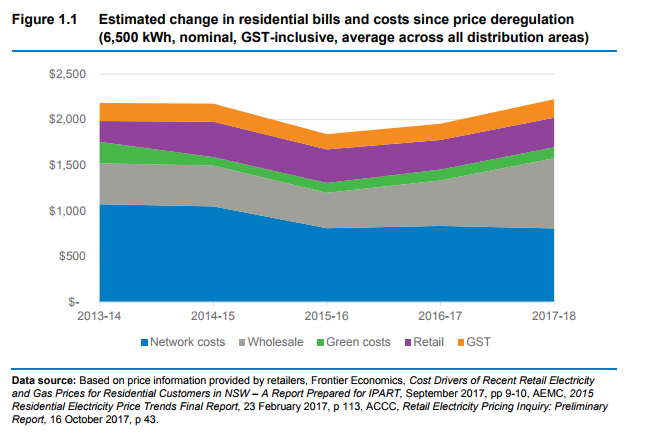

Also this week, the NSW regulator, IPART released its draft report from a review of the performance and competitiveness of the retail electricity market in NSW. It found that average annual bills for residential customers in that state are currently around the same as they were in 2013-14 before prices were deregulated. As the chart below shows, NSW network prices have declined materially over the last four years. For example, network prices fell by between 12% (Endeavour’s network) and 35% (Essential Energy’s network) in 2015-16 for residential customers.

Review of the performance and competitiveness of the retail electricity market in NSW. IPART, October 2017

In Victoria, electricity distribution costs have been relatively steady. Based on an independent analysis by Oakley Greenwood, Victorian distribution networks note that their costs are lower in 2017 than they were in 2001. In fact, because other cost categories have increased relative to network charges over this period, the contribution of distribution charges to the average residential bill in Victoria have fallen dramatically from 42.7 per cent of the bill in 1995 to 25.4 per cent of the bill in 2017.8

Nationally, it’s also relevant to note that the AER’s revenue and pricing determinations made in 2012–15 provided for maximum revenue that networks can recover from customers, which is on average 9 per cent lower than recoverable revenue in the previous regulatory periods.

Getting the future right will pay off

The ACCC report notes the future facing work of the Energy Networks Australia-CSIRO Electricity Network Transformation Roadmap released earlier this year.

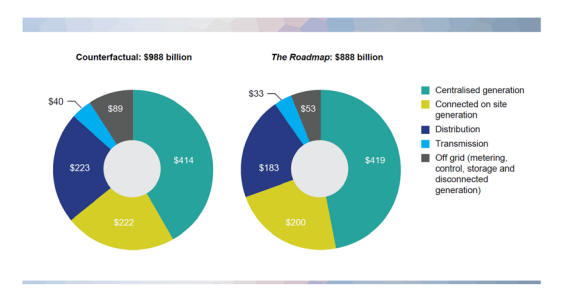

Roadmap analysis shows that we can avoid up to $16 billion in extra costs, reducing network charges by 30%, but it will require pricing reform, incentives and a modernised electricity system to realise the full value of the fleets of distributed energy resources being connected to the system.

The whole of system savings which can be achieved are material to customers. The Roadmap finds there is the potential to achieve significant customer savings of approximately $414 per annum by 2050 with proactive measures by the energy networks industry and other market participants, enabled by efficient market and regulatory frame works.

The Roadmap identifies two primary sources of savings: The first is that reformed prices, incentives and distributed energy resources network optimisation deliver a reduced need for expenditure on network capacity replacement or expansion. The second source of lower bills is a more efficient utilisation of capacity, because the cost of each unit of capacity is recovered from a larger customer base.

Cumulative electricity system total expenditure to 2050 (in real terms) under the Roadmap and counterfactual scenarios[4]

Customers will increasingly drive savings, and shopping around pays

The ACCC report also reinforces the critical message that customers can take control over their energy bills through shopping around. The AER has previously estimated an average NSW household could save up to $77 per annum by switching to the average market deal. The ACCC finds there is a lack of awareness of the tools available to assist customers, such as the AER’s Energy Made Easy website and the Victorian Government’s Victorian Energy compare.

The report also brings in focus the benefits that many Australian households have enjoyed from residential feed-in-tariffs and falls in solar installation costs, but that others are not able to access this, which is an equity issue.

“…. the ACCC is concerned that too little regard has been given to the affordability and distributional impacts of certain policies. The best example of this is premium feed-in tariffs which were costly and distortive in that some electricity customers benefited, while others were burdened …”[5]

Future schemes that will impose costs on electricity customers should be rigorously and transparently analysed. In particular, policymakers must ensure that the costs created by environmental schemes are not disproportionate to the benefit they seek to achieve and cross-subsidies should be avoided, particularly where they disproportionately affect those least able to pay.

Ensuring retail market passes through savings

It is critical that customers have the supportive market and competitive structures to ensure falling network costs are passed through to them.

The ACCC report makes the point that in a competitive market environment, we should not necessarily expect network costs to always be a simple pass through for energy retailer. The report notes:

“However, we note that not all retailers necessarily treat network costs as a one for one cost pass through. Some retailers expressed difficulty in providing disaggregated network cost data to the ACCC. This indicates that for these retailers, changes in network prices do not necessarily directly translate into changes to the retailer’s tariffs. These retailers may adopt different pricing methodologies rather than using a bottom–up cost stack methodology.”[6]

Energy retailers should be as incentivised as possible to pass on the network efficiency gains to their customers, as quickly as they occur. Reform should focus on ensuring that the retail market delivers responsive pricing outcomes, allowing customers to benefit from the efficiency gains made by networks, and that the potential for uncompetitive retail markets to dilute these customer gains is reduced.

What is next?

As we consider the roll out of the Australian Government’s National Energy Guarantee the ACCC Report provides important context about historic trends that might inform our future action. Key questions for networks businesses are, given the lessons of the past, how can we ensure that future reliability and security measures do not come at excessive cost? Importantly, what role do networks have in contributing to the reliability of the grid? In particular, what can be done to ensure that storage or other demand management options are available? How would this sit with existing regulatory structures?

However, an area for further consideration by the ACCC may be reviewing its approach to assessing network costs. Energy network businesses have rightly pointed out that the averages featured in the ACCC’s report can hide more than they reveal. As Victorian distribution network, United Energy has pointed out, it has delivered enhance network services, three times greater reliability for prices to customer that are 25 per cent below 1995 levels.

There will be many of these network–by-network realised customer experiences that don’t match the ‘nationally averaged’ headline findings of the report and there is a need for policy responses to the ACCC’s review to recognise this diversity in network and customer experience.

[1] ACCC, Retail Electricity Pricing Inquiry Preliminary report, 22 September 2017,Figure 2.35 (p.64)

[2] ACCC, Retail Electricity Pricing Inquiry Preliminary report, 22 September 2017, Figure 2.33 (p.62)

[3] ACCC, Retail Electricity Pricing Inquiry Preliminary report, 22 September 2017, Figure 2.37 (p.70) and Figure 2.30 (p.56)

[4] Energy Networks Australia and CSIRO, Electricity Network Transformation Roadmap, (2017),p 9

[5] ACCC, Retail Electricity Pricing Inquiry Preliminary report, 22 September 2017, p153

[6] ACCC, Retail Electricity Pricing Inquiry Preliminary report, 22 September 2017, p 65