How electricity became a headline CPI act

Last Wednesday the Australian Bureau of Statistics (ABS) released the latest Consumer Price Index (CPI) figures. They showed that the national CPI rose 0.6 per cent in the September quarter 2017.

Why is this an energy issue?

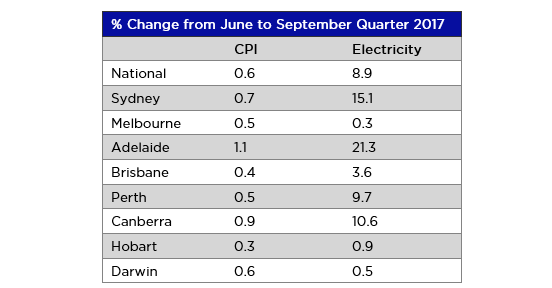

The most significant CPI rise this quarter was electricity (+8.9%). The underlying contribution of electricity varied significantly across the eight state capitals.

The table below shows the all groups and electricity CPI changes by city.

Source: 6401.0 Consumer Price Index, Australia, TABLE 11. CPI: Group, Sub-group and Expenditure Class, Percentage change from previous quarter by Capital City and TABLES 1 and 2. CPI: All Groups, Index Numbers and Percentage Changes

What is behind these increases?

The recent ACCC Preliminary Report on Retail Electricity Pricing found that over the last ten years network prices were the largest contributor to rising prices.

One concern Energy Networks Australia has raised with the ACCC report is that some of its data is dated, only including the period up to 2015-16.

A range of market and government policy factors that drove network cost increases from 2007 to 2012 have since moderated or been addressed, with significant changes in market conditions, government reliability standards and regulatory frameworks. In the AER’s current revenue and pricing determinations, revenue that networks are forecast to recover from customers is on average 13.5 per cent lower than recoverable revenue in the previous regulatory periods.[1]

So, with the new CPI data showing an 8.9% increase in the cost of electricity in a single quarter, it is worth examining the cause of the recent price spike.

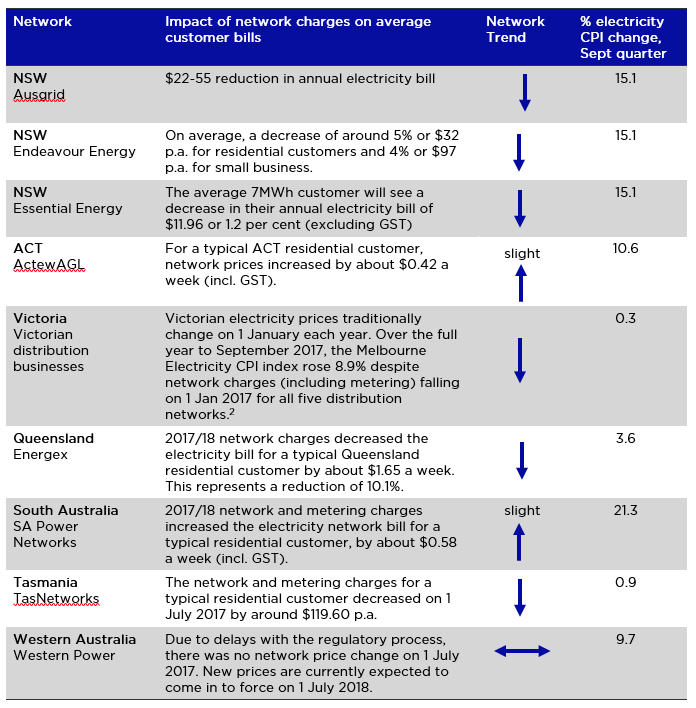

The table below shows the movement in electricity network prices on 1 July 2017 compared to the electricity CPI change.

So while the CPI was rising over the last quarter, network costs have either decreased or remained flat in most jurisdictions. Small increases were recorded in the Australian Capital Territory and South Australia.

The recent IPART Review of the performance and competitiveness of the retail electricity market in NSW found that in NSW

“electricity retail prices increased by an average of 14% for residential customers, and between 10% and 16% for small business customers at the start of 2017-18. This large price increase reflects the change in the underlying costs of supply – in particular rapidly increasing wholesale costs”[3].

IPART goes on to say that

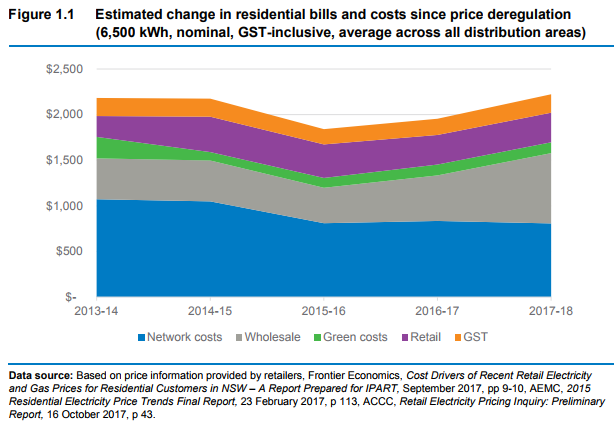

“the average annual bills for residential customers in NSW are currently around the same as they were in 2013-14 before prices were deregulated, and are slightly lower in real terms….this is because the increases in wholesale costs in 2016-17 and 2017-18 have been largely offset by falling network costs and green scheme costs in 2014-15 and 2015-16. For example, network prices fell by 12% (Endeavour’s network) and 35% (Essential Energy’s network) in 2015-16 for residential customers (see Figure 1.1 below).

If networks aren’t the cause, what is?

In a word, Hazelwood, or as the ABS commented

“increases in wholesale prices were passed on to consumers. Increases in wholesale prices have been observed across the National Electricity Market (NEM), with the most significant rises this quarter in electricity being observed in Adelaide; Sydney; Canberra and Perth.”[4]

The closure of Hazelwood with just five months’ notice in March 2017, has had a material impact on forward wholesale prices and much of this flowed through to retail consumers in the September quarter.

What to do to address this is a complex question.

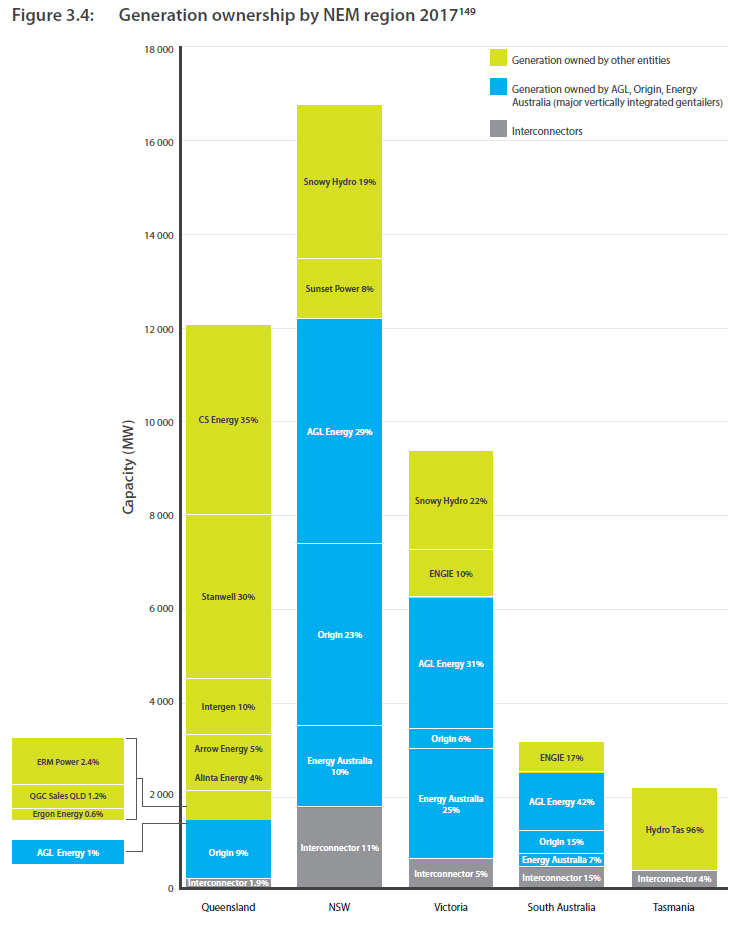

In the period from 2009 to 2017, the major retailers have increased their share of NEM generation capacity from 15 per cent to 48 per cent[5]. The Finkel Review indicates generation ownership by NEM region in 2017 as shown below.

The graph shows significant generation concentration in several jurisdictions. The ACCC recently commented that “the wholesale (generation) market is highly concentrated and this is likely to be contributing to higher wholesale electricity prices”[6].

As review after review into the energy sector has found, there’s no silver bullet to fixing rising power prices. However, these reviews also consistently point to a common opportunity – the implementation of nationally consistent energy and climate policy that lasts beyond a single election cycles.

[1] Australian Energy Regulator, State of the Energy Market 2017, p.14.

[3] IPART (2017) Review of the Performance and Competitiveness of the Retail Electricity Market in NSW from 1 July 2016 to 30 June 2017, Draft report October 2017, p. 2.

[4] ABS Media release: Inflation rose 0.6 per cent in the September quarter 2017

[5] Australian Energy Regulator, State of the Energy Market 2017, p.47.

[6] ACCC press release: Electricity report details affordability, competition issues available