A platform for the household energy revolution

Australia is often called a world leader in consumer energy, as 15% of households have rooftop solar PV installed, and some States have penetration rates above 30%. The Electricity Network Transformation Roadmap program undertaken by CSIRO and Energy Networks Australia forecast that Solar PV could increase by a further 500% in the next decade, while battery storage could increase to 34,000 MWh over the period. By 2050, over 35 per cent of all electricity could be generated by customers with payments to over 10 million distributed energy resources (DER) participants for network support services, instead of building traditional poles and wires.

The Roadmap program has been informed by global leaders in energy transformation, with a particular focus on United States market reforms. The Program has just released a new report synthesising key conclusions on approaches to integrating DER: ‘Future Market Platforms and Network Optimisation: Synthesis Report’.

Modernising the grid

With high levels of DER penetration, the distribution grid will become far more operationally complex. An energy system built for one-way energy flows from utility-scale generators to end use customers will now cater for greater variability and more multi-directional flow patterns.

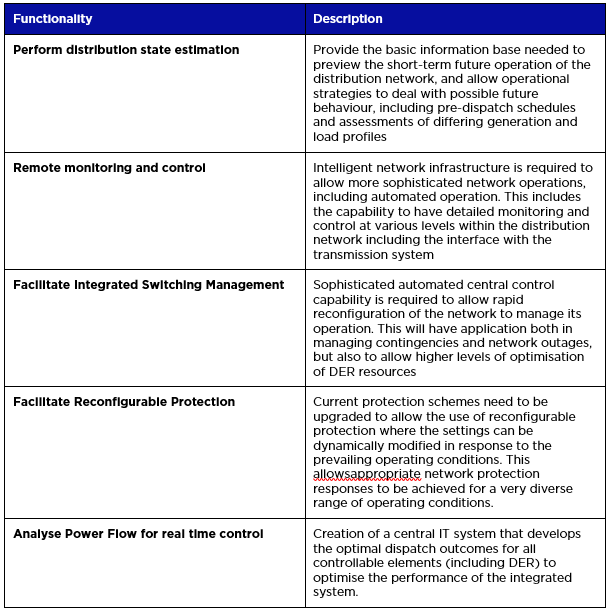

Network businesses are evaluating grid modernisation and new operational practices, justified on customer value. Significant changes will be required in the way the network is planned, in developing and using forecasts and utilising smarter controls, monitoring and operations. Victoria’s smart meter deployment is already demonstrating the benefits to customers of a more actively managed smart grid to improved outage responses, efficient network operations and provide an improved customer service[1]. However, more work will be required by Networks to establish key functionalities.

For networks to actively manage distribution grids in the future, they will require enhanced analytical capability, including the capacity to model the DER and its characteristics for forecasting and planning purposes in an optimised network.

California’s Public Utility Commission has already required networks to prepare Distribution Resource Plans informed by assessments of integration (or ‘Hosting’) capacity which identifies locations where DER can be added without the need for additional network support and/or augmentation; and the locational value of DER. Proposals are required for demonstration projects for Distribution Operations at High Penetrations of DER; and DER Dispatch to Meet Reliability Needs.

New systems will be required for forecasting and managing the interface between the transmission and distribution systems, as variable renewable generation becomes prevalent at all voltages. At the transmission system level, DER represents millions of individual potential supply points which are currently invisible and unpredictable to the transmission system operator or AEMO[2].

The report identifies a number of conceptual models which may bridge the gap in the future between transmission system operations and high penetrations of DER, including: Total Transmission System Operations; a Distribution Managed Interface; or Oversight of DER by Distribution Network Operator.

As identified in the US and other countries, it is essential as a starting point that distribution network operators have visibility of the physical operation of DER if it is being used within the bulk supply market. The physical coordination of DER schedules and dispatch by AEMO and DER providers needs to be known by the distribution network operators to ensure that it can be accommodated efficiently over the distribution network. On the other hand, AEMO needs much more accurate information and forecasts of the likely loading at each connection point, including an estimate of changes to allow it to effectively operate the transmission system. [3]

Future markets

The Synthesis Report highlights not only the challenge of Grid Modernisation, but the opportunity to unlock the full value of DER with the right market models. DER owners are likely to face a range of offerings from aggregators (including retailers), networks and other parties seeking to rely on the DER’s ability to deliver real and reactive power within certain time windows. The best outcome for customers naturally requires serving multiple value streams with the same DER asset. For instance, commercial structures should allow DER services to be procured with requisite firmness to achieve network efficiencies, without precluding other services such as energy market arbitrage or ancillary services that DER owners or aggregators can seek across the electricity value chain.

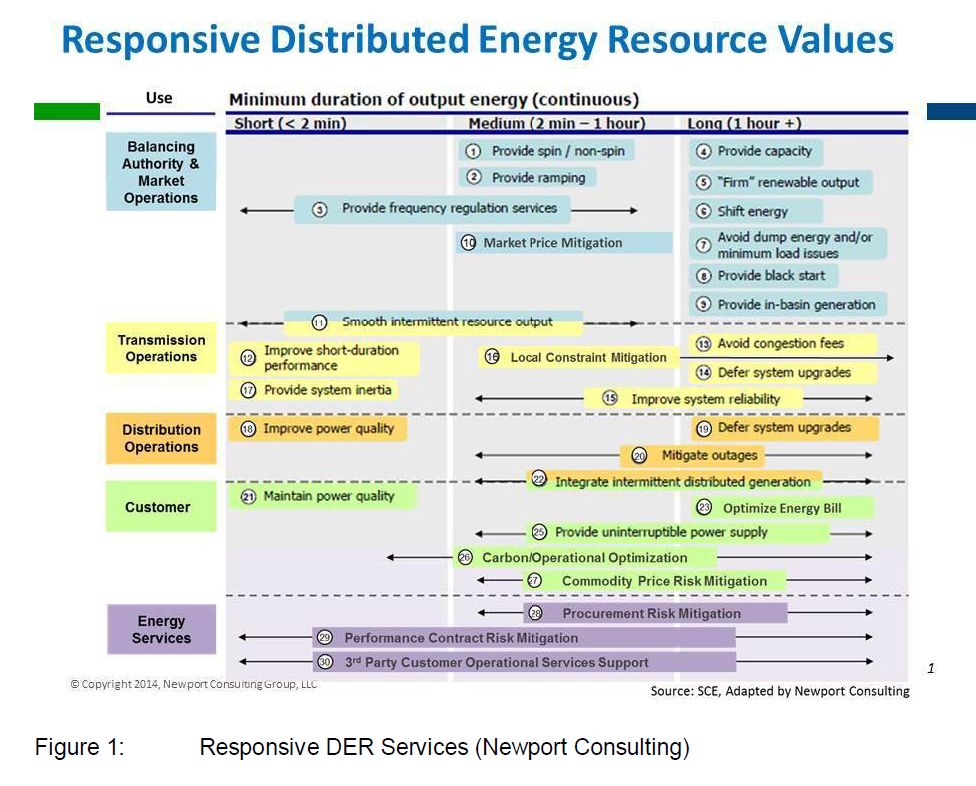

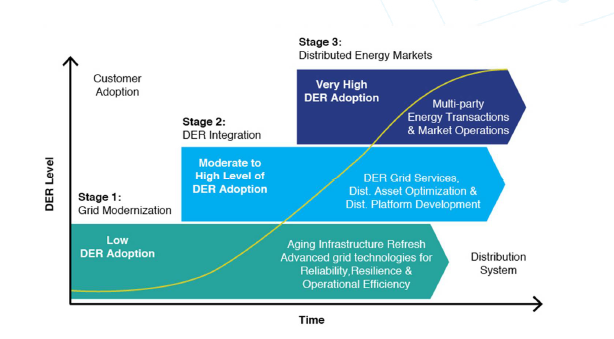

Many Australian electricity networks are already procuring, or trialling, the use of non-network solutions in lieu of traditional poles and wires solutions. Such initiatives are usually premised on long-term procurement frameworks so that the network deciding not to invest in a poles and wires solution (such as for network augmentation in a growth area) is assured of an equivalently firm DER outcome that meets service obligations to customers. The Synthesis Report highlights the potential development of a Network Optimisation Market (NOM) which would provide a commercial framework could take a number of different forms, and may be subject to a staged development process. Figure 1 (developed by Newport Consulting) illustrates the potential staging of changes to distribution network operations to implement the desired transition.

Figure 2. Transition of Network Operations to cater for DER (Newport)

Initially a NOM may involve simple contracting or bulletin board approach to procurement over longer time scales, rather than a dynamic market. This would provide simplicity with low transaction costs but is only likely to be able to be accessed by large or aggregated fleets of DER resources.

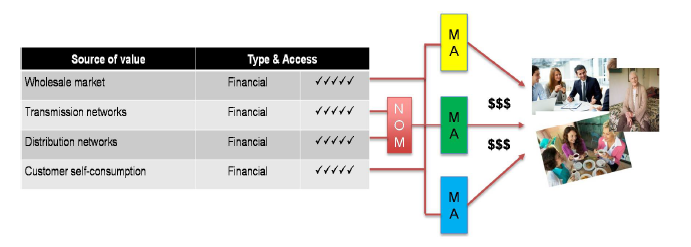

Figure 3. A Network Optimisation Market unlocks network value streams to be bundled by various Market Actors (MA).

While each stage of development would require its own business case justification, consideration could be given to a more dynamic NOM with increasingly granular transactions at increased volumes from smaller and smaller DER sources. This digital Network Optimisation Market (dNOM) creates the potential for near real time or automated trading of DER services, which could unlock system stability or power quality services of DER.

A ‘dNOM’ would involve higher transaction costs and the capability to support large numbers of market participants, data volumes and transactions, with standardised specifications and contract terms. The parties buying and selling DER network-optimisation services would rely on highly automated digital procedures for service matching and market clearing. The USA’s GridWise Architecture Council has identified the need for such systems to be:

- Coordinated and self-optimising: The system must seamlessly enable distributed energy resources fleet ‘orchestration’ and self optimisation at the customer level;

- Technical and economic benefits: The system must enable the integration of distributed energy resources in a way that supports both power system reliability and economic efficiency;

- Firmness of response: The system must be designed to ensure firmness of response from distributed energy resources at all critical times (with equivalent certainty to traditional network augmentation where it is relied on to avoid that expenditure);

- Non-discriminatory: The system must provide for non-discriminatory participation by qualified participants;

- Transparent: The system must ensure the value of network optimisation opportunities is transparent and the benefits are received for actual distributed energy resources services provided;

- Verifiable: The system must be observable and auditable at its interfaces; and,

- Future proof: The system must be scalable, adaptable, and extensible across a number of devices, participants, and geographic extent.

The Roadmap Key Concepts Report recommended that the Network Optimisation Market be progressively implemented over the coming decade, enabled by a range of grid modernisation measures. By 2027, the Roadmap found there should be sufficient experience in DER procurement, active development of DER markets and orchestration services to allow the feasibility of a digital platform, or dNOM to be assessed.

Next steps

Industry and governments can work together to capture the benefits of the household energy revolution for all. The Electricity Network Transformation Roadmap provides a pathway to unlock the full potential of Australia’s DER to keep the lights on, bills affordable and decarbonise electricity.

The Roadmap Final Report will be launched on Friday 28 April, 2017. You can register for the webinar here

[1] Future Market Platforms and Network Optimisation: Synthesis Report

[2] Future Power System Security Program: Progress Report, AEMO

.jpg-autosave")