The Fall of Bonds: Never Say Never Again

This week the Reserve Bank of Australia announced the first tentative steps to reduce the size of one of a number of unprecedented monetary policy measures it adopted to seek to boost the economy during the initial phases of the COVID-19 pandemic.

Every two minutes of every day and night since early November 2020 until this week, the Reserve Bank of Australia has been purchasing the equivalent of about $1 million in government issued bonds in the market, as part of a policy objective of driving interest rates lower. As a result, this month it owns about $156 billion of government bonds. From this week, the RBA has announced it expects to be buying approximately $4 billion a week – or $570 million every day.

Reviewing approaches as markets take a back seat to recovery measures

Even before the onset of the pandemic, globally interest rates had hit all-time lows. In some countries, negative interest rates and trillions of dollars of negative yielding debt had emerged as financial authorities sought to stimulate economies and hit their inflation targets.

Critical regulatory decision-making impacting on customers and networks is currently in the process of colliding with these new economic realities.

The Australian Energy Regulator (AER) has the challenging task over the next eighteen months of stepping into this unusual set of conditions and setting out a standardised approach for estimating the rate of return on more than $100 billion of gas and electricity network infrastructure.

This scheduled review seeks an appropriate way to estimate the cost of funds – or rate of return – for investments in new and existing poles, wires and distribution pipelines that provide energy and critical grid access to millions of Australian customers.

Falling off a plateau – the changing bond environment puts models under stress

It is a very different environment from that in which past rate of return approaches were determined.

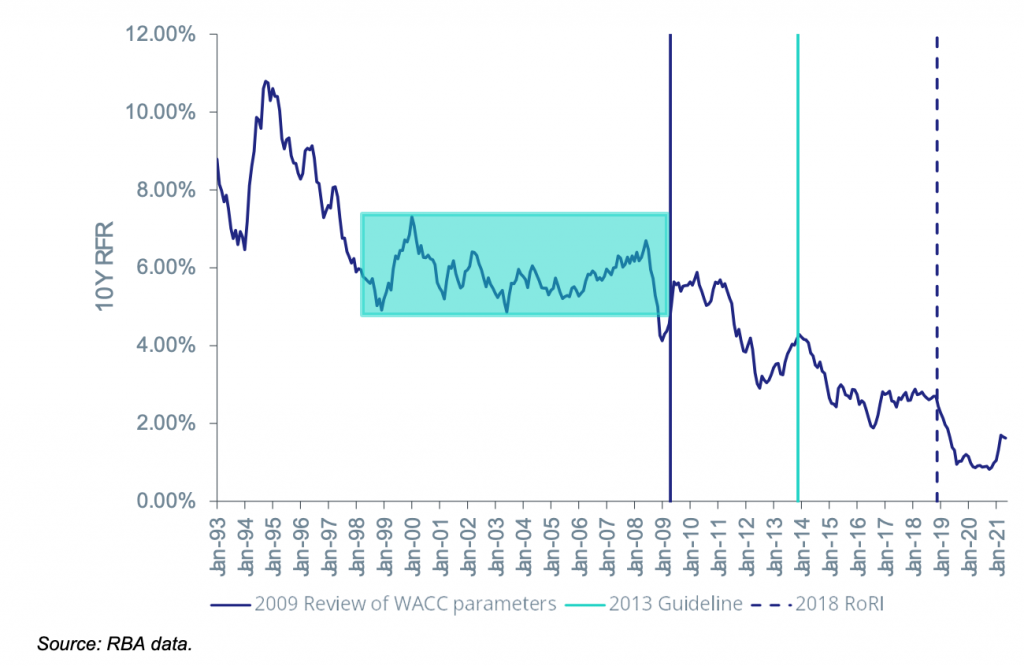

In fact, the design and formation of Australia’s modern energy regulatory framework, from about 1998 to 2008 saw a relatively stable set of interest rate conditions by comparison. This can be seen in the shaded area in the chart below.

Figure 1 – Movements in 10-year government bond yields over time

Since that relatively stable period, bond yields have collapsed. Following the AER’s last rate of return review in 2018 bond yields have declined proportionally much more sharply than following any previous comparable guideline.

This is important because regulators such as the AER typically build these regulatory return estimates on a “base” of what is called the ‘risk-free’ rate – and have traditionally used the 10-year government bond rate in setting this risk-free rate.

Under the AER’s current approach, the regulatory return on equity for investors is set in each five-year network pricing decision by adding a risk premium of 3.66 per cent to an average of recent yields of 10-year government bonds.

Customers have rightly collectively benefited by billions of dollars through lower network prices at each network determination from this trend of falling interest rates. Yet, the simple reality is, there may be not much further to fall, and the decline to historically low bond yields puts this approach under stresses never contemplated in its design, or in previous AER rate of return decisions.

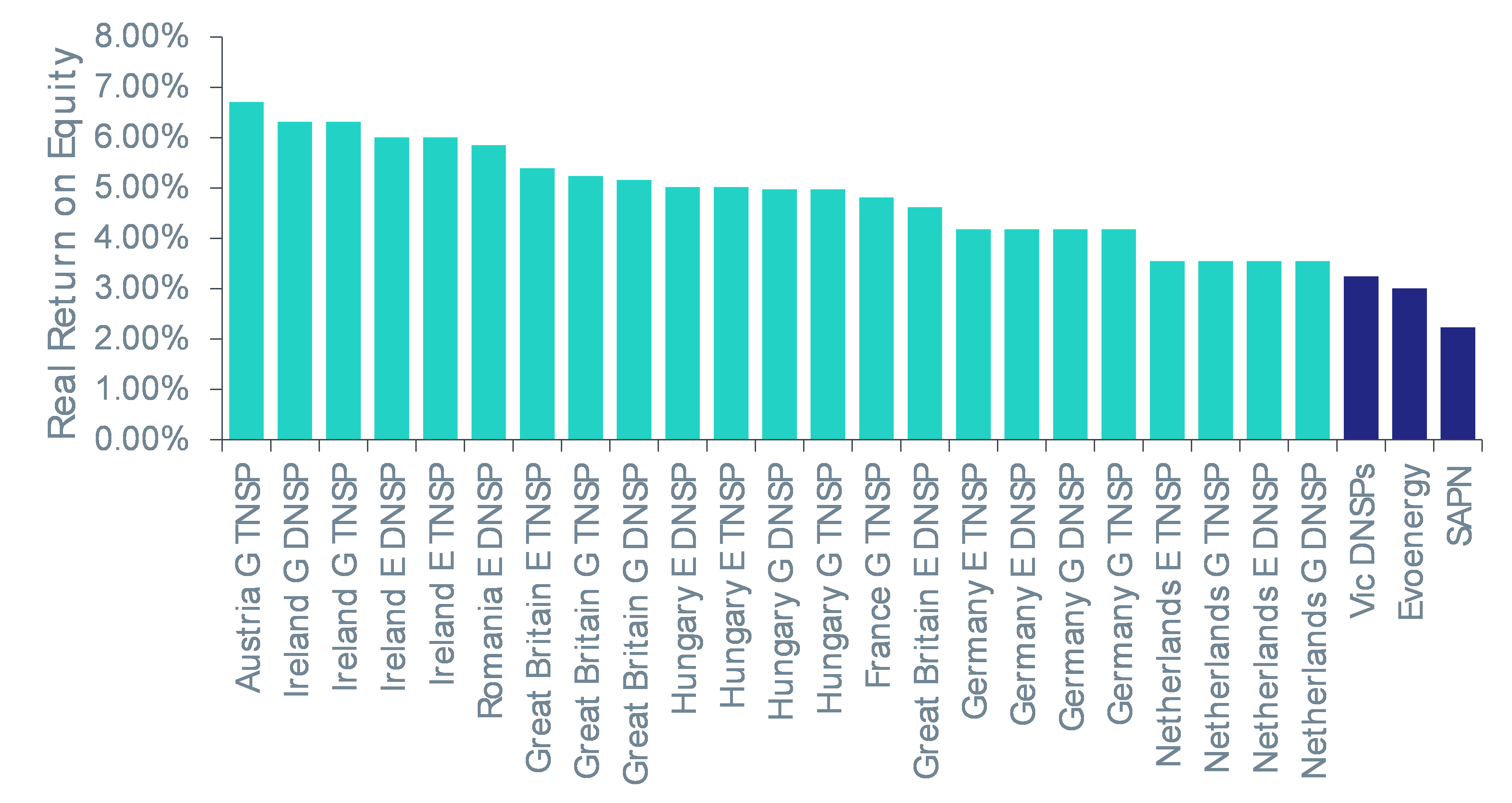

It has contributed to historically low return of equity allowances – below those of other international regulators – who adopt a variety of different approaches.

Figure 2 – International regulatory rate of return allowances – real returns on equity

The question being discussed in the lead up to the next rate of return review is whether and how should AER approaches potentially adapt and change to recognise these unprecedented conditions?

Emerging issues – accounting for monetary policy interventions and alternative approaches

There is no shortage of significant issues for the AER to consider.

The risk-free rate is supposed to be a market determined rate, yet the RBA currently holds 20 per cent of all government bonds and it expects to own about 30 per cent by later this year.

The RBA estimates these deliberate policy interventions are pushing yields lower by at least 0.3 per cent. It also expects its interventions to have a long-term impact on bond yields, even where current measures are wound back.

The question of what makes up a good base – or ‘risk free’ proxy – for the AER to use in its future decisions is also coming under increasing question following changed approaches from overseas regulators.

Some international infrastructure regulators use generally more stable longer-term bonds (such as 20 or 30-year government bonds) which better reflect the life of the regulated assets.

The UK Competition and Market Authority has also recently revised its approach to estimating the risk-free rate – rejecting past assumptions that the risk-free rate simply equals the government bond rate as unrealistic and flawed. A revised approach has been implemented in the water infrastructure sector, and potentially might also apply in the future to energy network infrastructure.

While rates are low, the stakes for customers are high

Setting regulatory rates of return across more than $100 billion of energy network infrastructure is one of the most consequential individual decisions made for customers in the Australian economy.

It determines long-term incentives for network investments that underpin current and future customers’ access to reliable energy supply. It is one of a number of factors – alongside wholesale market prices, energy retail margins and recovery of costs from government schemes – that affect final energy prices.

More than ever before network investments are directed at enabling the value of customers’ distributed energy resources – such as behind the meter solar or batteries – to be fully realised for the benefit of customers and the community alike.

Similarly, in electricity transmission, a key driver of investment needs is bringing new abundant wind and solar resources to the wholesale market, driving down prices for customers.

This is a marked change from just a decade ago, where network investment was much more focused on building infrastructure to simply meet customers demand for energy.

Efficient investment which does not proceed today is more likely than previously to represent a missed opportunity of bringing greater energy supply to wholesale markets, supply that brings with it greater grid resilience, reduced wholesale costs and improved reliability.

This means the stakes for the decisions the AER alone is charged with making are arguably higher than ever before. Wherever interest rates and future monetary policy might go in the future, these stakes remain.