A British take on future energy regulation

Network investment is essential to drive the clean energy transition. One challenge being experienced globally is how to unlock a regulatory framework that allows for prudent, timely and efficient investment to support this transition.

We look at how the UK plans to tackle the issue in Ofgem’s Consultation on frameworks for future systems and networks regulation: enabling an energy system for the future[1].

Background

The UK aims to achieve net zero by 2050 and a 78 per cent reduction in carbon emissions by 2035. Britain is much more reliant on gas for heating than Australia, which has led to a more mature focus on development of Hydrogen to decarbonise the gas market. By 2030, the UK Government plans to reach a target of 10GW of low carbon hydrogen production capacity.

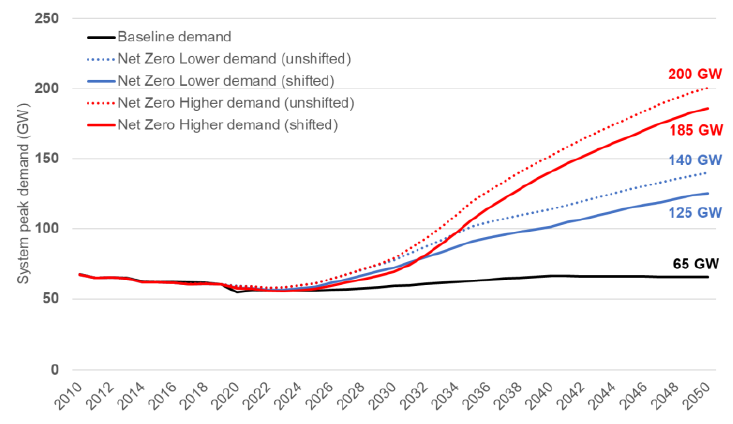

The UK energy transition, like in Australia, relies heavily on investment in networks to link up new sources of clean energy from new locations. A focus in Ofgem’s consultation paper is how to anticipate future demand and having the right infrastructure in place before it is needed. Future demand in the UK is anticipated to be two to three times more than peak demand today, as outlined in Figure 1. Network investment needed to meet future demand will cost £20-27bn in investment in the 2030s alone.

Figure 1: UK Future Energy Demand

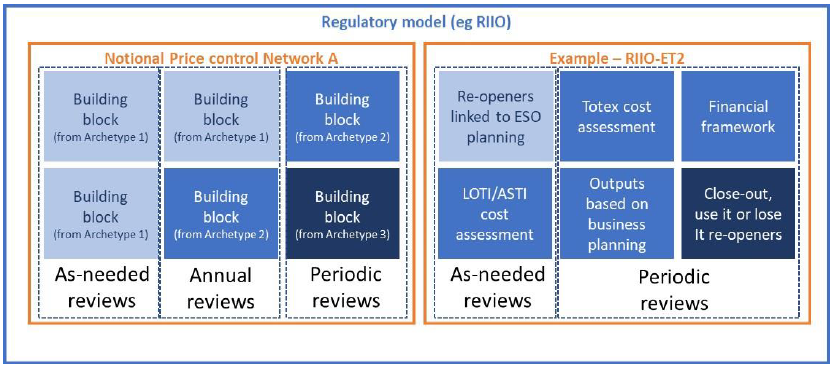

To drive the change Ofgem proposes the use of three so-called “archetypes” for future network regulation. An archetype represents a set of tools used to assess different components of network development proposals. Figure 2 provides an example of when the proposed archetypes would apply.

Figure 2: Archetypes and their application in building regulatory building blocks

Archetype 1: ‘Plan and Deliver’

To create a future proofed system, the first archetype overcomes the issue of information asymmetry. The consultation proposes an external system planner who determines a need and the most efficient delivery model for new investments and upgrades, transforming national and regional strategic plans into clear and detailed descriptions of network requirements. Under this plan a Future System Operator (FSO) in the UK would develop a new Centralised Strategic Network Plan (CSNP) as the first stage in strategic planning. The goal is to produce something like the Australian Energy Market Operator’s (AEMO) Integrated System Plan (ISP)[2] or Ontario’s Annual Planning Outlook[3] in Canada.

Under this archetype, Ofgem sees its role transitioning away from upfront cost assessment and monitoring of efficient delivery and towards identifying the need and process that provides the best outcomes at the most efficient cost.

Archetype 2: Ex ante Incentive Regulation

The RIIO-2 is the UK’s current iteration of its incentive regulation approach. Ofgem’s consultation suggests the RIIO-2 needs to change alongside the new delivery plan, presenting two options for incentive evolution. Development of incentive regulation for ‘one-off’ investments is ongoing.

The first option is a simplified regulatory framework such as efficiency incentives based on reducing costs relative to an adjusted baseline, just like the system here in Australia. Ofgem suggests these systems could be suitable to business as usual (BAU) activities that are repeated over time and are less subject to dealing with uncertainties, potential biases towards capex over opex, the need to promote innovation, or the use of targeted outputs to drive improvements in performance.

Second, is to increase the use of ‘ex post’ (or after the fact) productivity-based cost assessment mechanisms. This would apply to BAU activities, but also to where there is a measurable change in outputs of the network over time, like benchmarking on actual out-turn expenditures and realised efficiencies.

Archetype 3: ‘Freedom and Accountability’

Under this archetype, Ofgem proposes to no longer set upfront targets for costs and efficiency or require detailed plans for network investments. Ofgem would instead determine and provide guidance on monitoring the outputs to simplify the upfront regulatory process. Licensees would then decide on the most efficient delivery model to achieve identified outputs. Following completion, Ofgem would review the licensee’s investment performance and provide a reward or penalty.

To avoid incentivising ‘gold-plating’ of assets, Ofgem suggests this method would be best used for circumstances where there is limited scope for over-investment. Incentive regulation, like the use of ex post measured efficiency or reducing permitted rates of return for inefficient investment, could push networks to continue striving for cost-reducing innovation.

Examples of the ‘archetypes’ model in practice

Electricity Transmission

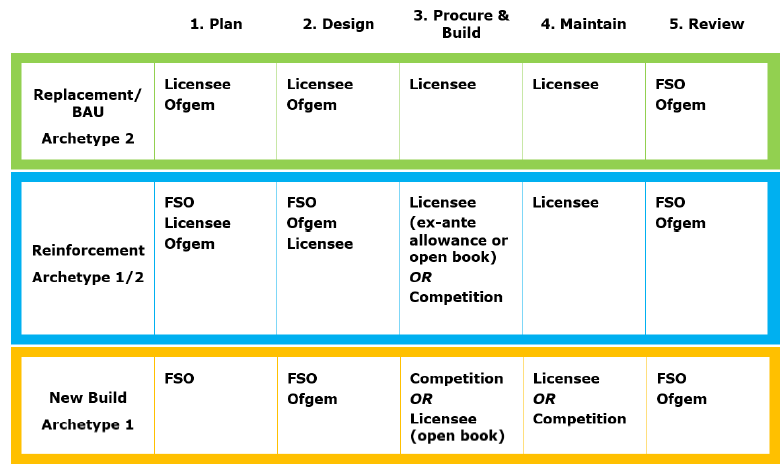

Figure 3 outlines how archetypes would apply for electricity transmission. Ofgem proposes archetype one applies for new builds due to planning phase being dominated by the FSO. Archetype two mechanisms would apply for BAU/replacement investments, with plans submitted by licensees. Both archetypes one and two could be used for reinforcement activities as the planning for large projects is dominated by the FSO, but for smaller projects other small-scale evaluations and business plans might be more appropriate.

Figure 3: Electricity Transmission Example Model

Electricity Distribution

Ofgem considers the distribution network to be more likely disrupted by distributed energy resources (DER) over time and will require more innovation than transmission. Ofgem suggests regulatory models will need to allow for new entrants to propose new solutions which may not currently be clear to the FSO. Ofgem also recognises the need for granular time-based and locational data that can unlock innovation and optimise system planning.

An alternative form of incentive regulation to RIIO-ED2 does not need to be in place until 2028, however, consideration has been given to the possible application of archetypes one and three.

Gas Transmission and Distribution

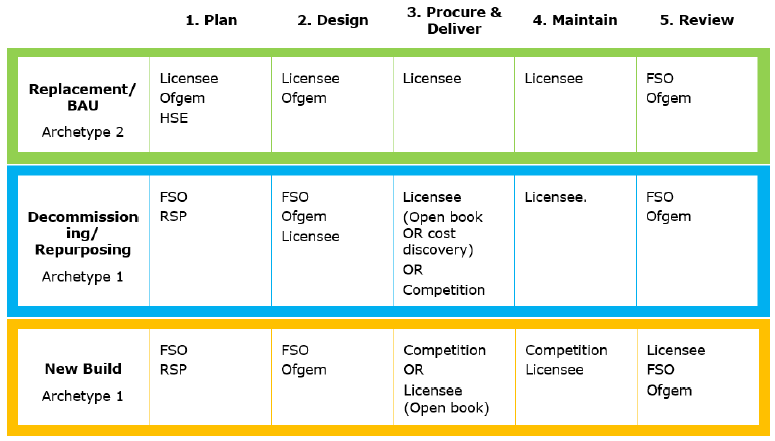

Figure 4 outlines how each archetype could apply to gas activities. The planning and design for decommissioning and repurposing activities is proposed to work under archetype one through the FSO-whole system planning approach. However, due to uncertainty in the costs of these activities, archetype three may be more appropriate.

Archetype one is proposed to be the model for new methane networks if they are needed and the UK Government is developing a separate business model and regulatory framework for hydrogen networks.

Figure 4: Gas Transmission and Distribution Example Model

Australia has often looked to the UK for inspiration in some of its regulatory developments. The moves to further evolve the UK model provide policy makers, regulators and the community to consider strategically where the type of regulation may need to evolve to meet the future transition task.

These issues will be further explored by the keynote speaker, Akshay Kaul Director of Infrastructure and Security of Supply, at ENA’s Regulation Seminar ‘New Horizons: Regulation and the Energy Transition’ in August this year.

[1] https://www.ofgem.gov.uk/publications/consultation-frameworks-future-systems-and-network-regulation-enabling-energy-system-future

[2] https://aemo.com.au/en/energy-systems/major-publications/integrated-system-plan-isp/2022-integrated-system-plan-isp

[3] https://www.ieso.ca/en/Sector-Participants/Planning-and-Forecasting/Annual-Planning-Outlook