Energy Innovation – Can the Grid keep up with its customers?

Federal Energy Minister Josh Frydenberg has described Australia’s electricity transformation as ‘the biggest change in the electricity system since the 1890s when Tesla beat Edison in the war of the AC/DC currents’. So why aren’t innovation incentives keeping pace in energy regulation?

The customer driven energy revolution will require electricity networks as agile as the technologies they connect. Australia has the opportunity to follow the example set by its global counterparts and improve customer outcomes by supporting network innovation and R&D more broadly through effective government schemes.

The UK comparison

Both Australia and the UK are debating how best to ensure innovation in regulated network contexts, although the two countries are at different stages of the debate. In Australia, current R&D support mechanisms for network innovation are limited.

In the UK, funding for network innovation has been in place since 2010. Having already provided £250m for innovative projects, the UK regulator Ofgem is prepared to approve further expenditure. Ofgem is also on the lookout for opportunities to further increase the value for money for consumers from its network innovation schemes based on what they have learned in the time the schemes have been in place. Scope and success of innovation projects has also benefited from the involvement of others outside of the industry.

Australia needs well-designed policies and approaches to support network innovation efforts, encourage progress of adventurous ideas and provide an environment where the risks of innovation can be managed. While funding provided to companies will ultimately be paid for by customers through their bills, customers stand to benefit from network innovation in the long run through decreased energy costs and improvements to valued services. The environmental benefits will also be realised by society at large.

Learning from the UK

The U.K. Office of Gas and Electricity Markets (Ofgem) recently completed a review of its first network innovation scheme. The Low Carbon Networks Fund allowed the industry to spend up to £500m on innovation. It has provided approximately £250 million ($425 million) of funding to projects sponsored by the six electricity distributors of Great Britain over the period 2010-2015.[i]

The cost of the scheme is significant – valued at approximately £1.7 ($2.9) per customer annually. [ii] However, an independent evaluation of the scheme concluded that the Low Carbon Networks Fund has delivered value-for-money. It is estimated that the roll out of successful projects across Great Britain could see net-benefits which are up to six times the cost of funding the scheme.[iii] Ofgem identified the total potential benefit of between £800 million ($1.3 billion) and £1.2 billion ($2 billion).[iv]

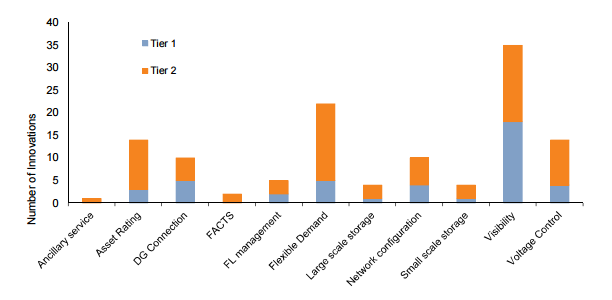

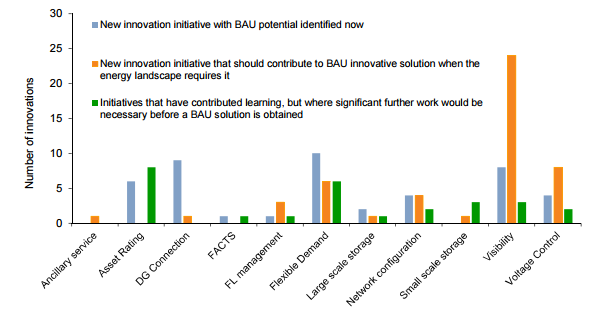

Innovations under the Low Carbon Networks Fund were considered to be relatively successful. UK Power Networks worked out the right mix of smart technologies to enable it to defer or avoid network reinforcement. (Flexible Plug and Play) Electricity North West has shown that substantial capacity can be unlocked using existing assets, without the need to expand the network. (Capacity to Customers)

Overall, nearly 40% of the initiatives have been successfully rolled into business as usual. Another 40% of initiatives are suitable for roll out once the business case can be established. The remaining initiatives require further development before being suitable for business as usual.[v]

Figure 1: Estimated number of innovation initiatives per category[vi]

Figure 2: Innovation initiatives by category and timing of BAU potential[vii]

Another success of the Low Carbon Networks Fund is embedding change and innovation within the operations of networks. The independent evaluation includes the following findings:

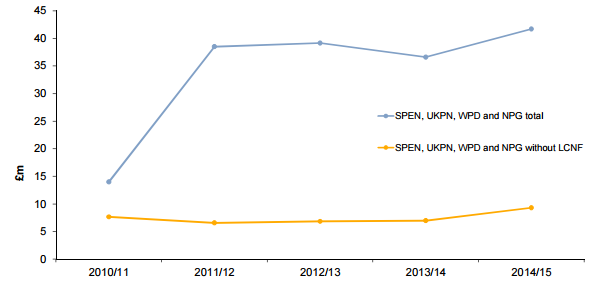

- The scheme has provided approximately £250 million ($425 million) of funding to innovative projects, when prior to its introduction the total expenditure on R&D by distributors was estimated to be less than £10 million ($ 17million) per annum.[viii] Spending on innovation in Great Britain is now greater than the EU average.[ix]

Figure 3: Nominal spend on R&D[x]

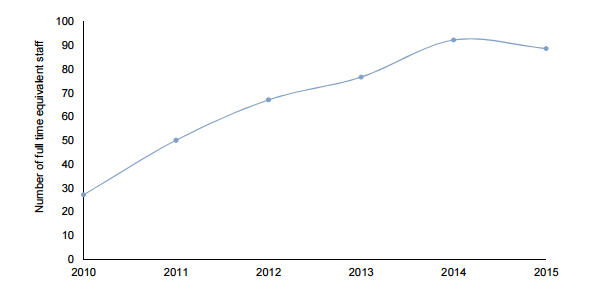

- Dedicated innovation teams have emerged within networks, suggesting that innovation is becoming a core part of their business. Over the period 2010-2015, the total number of technical staff in the Future Networks teams, for six distributors, increased from 27 to 90.[xi]

Figure 4 Growth in future networks technical staff[xii]

- Over the five year funding period, 23 large-scale projects and 42 small-scale projects have received funding under the scheme. 12 more projects were unsuccessful on their applications and were not funded.[xiii]

The independent evaluation recognised that even “failures” of innovation attempts can provide useful information.[xiv] The involvement of third parties has stimulated a greater number of innovative ideas and contributed to the success of projects.[xv]

Ofgem’s current innovation schemes

Ofgem’s most recent framework for the regulation of network businesses (termed the Revenue = Incentives + Innovation + Outputs, or RIIO) builds on the Low Carbon Networks Fund. This framework was introduced for gas distribution companies and electricity and transmission companies in 2013, and for electricity distribution companies in 2015.

Innovation stimulus consists of two innovation funding programs:

- The Network Innovation Allowance (NIA) provides partial funding for small innovation projects and covers all types of innovation. The NIA is available to each network business as part of their price control. The funding is set at £61 million ($103 million), and allocated based on the quality on the company’s own innovation strategy.[xvi]

- The Network Innovation Competition (NIC) is an annual competition to fund selected large-scale innovation projects which have the potential to contribute to meeting low carbon economy objectives. The annual funding available to a NIC winning project is capped at £90 million ($153 million) for electricity networks and £20 million ($34 million) for gas networks.[xvii]

Based on the independent evaluation of the Low Carbon Network Fund, Ofgem has made a decision to introduce some changes to the NIA and NIC. The changes are designed to make these even more effective and increase the benefits for consumers. In particular, Ofgem will reduce the level of funding for the electricity NIC from £90 million ($153 million) to £70 million ($120 million); and put new obligations on the networks companies to issue an annual call for ideas from third parties, and to jointly develop innovation strategies for the gas and electricity sectors.[xviii]

The schemes will remain in places until at least 2023.[xix]

The Australian experience

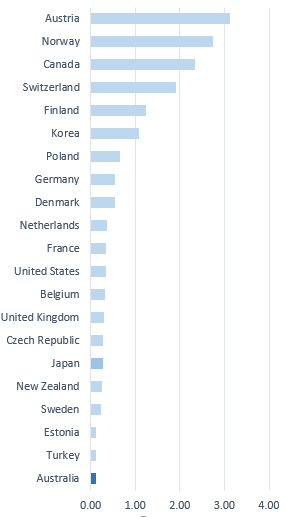

Australia’s spending on network innovation has been low compared to its international counterparts.

Figure 5: Electricity network RD&D funding per capita, USD (2015 prices and PPP), 2014

Source: Energy Networks Australia analysis, from IEA, Electricity transmission and distribution RD&D in million USD (2015 prices and PPP) per capita.

While Australia is at an earlier stage of the journey, there has been some progress. Electricity network businesses have been innovative in incentivised areas under the existing regulatory framework.

The main mechanism to encourage innovation by distribution networks is the Demand Management Innovation Allowance. In its past decisions, the Australian Energy Regulator (AER) allowed the recovery of between $0.1–1.0 million for various network firms. This measure has been the subject of a recent rule change, with the Australian Energy Regulator due to deliver a revised scheme by September 2017.[xx]

Broader capital and operating efficiency incentives included in the regulatory framework encourage innovation to some extent; however, their scope is limited. Incentives often focus on short-term projects aimed at containing costs and deriving operational efficiencies. Traditional expenditure tests may not be conductive to incentivising innovation. [xxi] Due to the inherent uncertainty of outcomes associated with innovative initiatives, it is often hard to demonstrate a priori that the proposed activities will satisfy the relevant criteria under the rules. Therefore, expenditure on cutting edge innovative projects is unlikely to be approved by the regulator.

Ofgem’s RIIO framework provides improved incentive properties for innovation, including through the adoption of the total expenditure or “totex” approach.

Seizing the opportunity

During a time of rapid technological change, Australia’s regulatory policy is yet to fully realise the benefits of innovation activities that are undertaken by network businesses and third parties, and that are valued by customers. This means that Australian electricity customers may miss out on the opportunities for integrating new technologies into grid that could improve the quality and reliability of electricity network services, and allow better responsiveness to customer choice in technology and service.

In light of recent trends in the energy sector, due to rapidly evolving technologies and business models, innovation in the delivery of network services may have substantial social benefit. Conversely, the absence of innovation will come at a cost.

As the experience of the UK shows, the operation of network innovation schemes includes a valid process of learning, adjustment, and refining. There is evidence that innovation schemes can deliver concrete benefits to energy customers. This should give Australia’s policy community confidence to trial and experiment with our own approaches.

[i] Pöyry, An Independent Evaluation of the LCNF, a report for Ofgem, October 2016, p.1.

[ii] Number of customers obtained from the Department for Business, Energy & Industrial Strategy, Electricity Statistics, Electricity: Chapter 5, Digest of United Kingdom Energy Statistics, p.126.

[iii] Pöyry, An Independent Evaluation of the LCNF, a report for Ofgem, October 2016, p.2.

[iv] Ofgem, The network innovation review: our policy decision, 31 March 2017, p.6.

[v] Pöyry, An Independent Evaluation of the LCNF, a report for Ofgem, October 2016, p.55-56.

[vi] Ibid, p.54.

[vii] Ibid, p.57.

[viii] Ibid, p105.

[ix] Ibid, p.106.

[x] Ibid, p.27.

[xi] Ibid, p.29.

[xii] Ibid. p.24.

[xiii] Ibid, p.6.

[xiv] Ibid, p105-106.

[xv] Ibid, p.29.

[xvi] Ofgem, The network innovation review: our policy decision, 31 March 2017, p.9.

[xvii] Ibid, p.9.

[xviii] Ibid, p.6.

[xix] Ibid, p.27.

[xx] AER, Consultation paper, Demand management incentive scheme and innovation allowance mechanism, p.7 and p.47.

[xxi] CEPA, Future regulatory options for electricity networks, August 2016.