Delivering net-zero emissions at half the cost

The latest Gas Vision 2050 report has shown net-zero emissions can be achieved with hydrogen at half the cost of electrification.

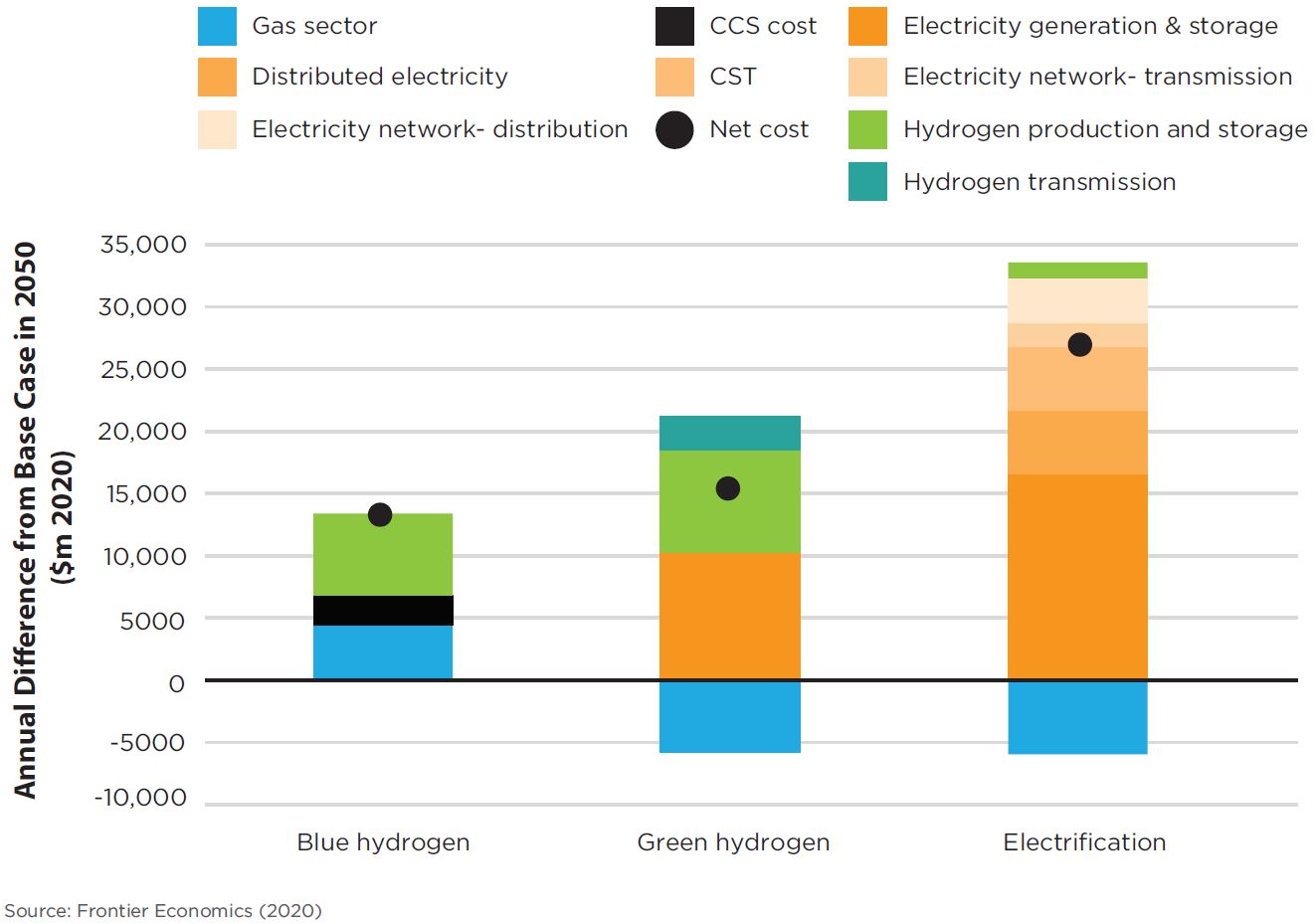

Figure 1: Cost comparison of net-zero pathways (Source: Gas Vision 2050)

Gas is already a clean energy source, and with the growth of renewable gas, it will become net-zero emissions, offering consumers an ideal fuel to balance the different aspects of the energy trilemma: energy affordability, energy security and environmental outcomes.

Figure 2: The Energy Trilemma (Source: Gas Vision 2050)

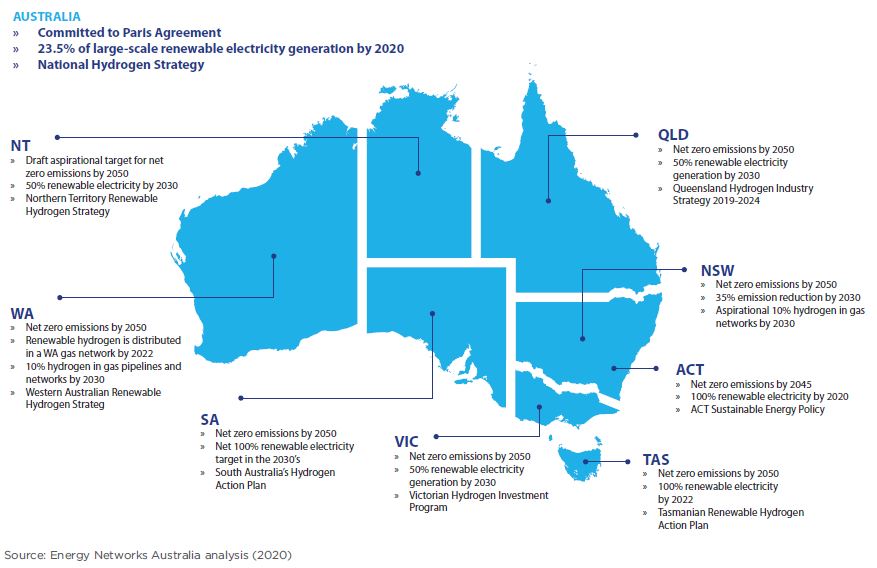

Australia is decarbonising its energy supply, and most of the progress to date has been in the electricity sector. There is an ongoing interest to increase the level of renewable generation with most of Australia’s state governments having established their own targets.

Figure 3: Hydrogen projects around Australia (Source: Gas Vision 2050)

Attention is now turning to decarbonising other sectors, especially the services provided by natural gas.

Customers have told us that they are interested in greener gas options and industry is responding by demonstrating a range of green hydrogen projects.

More than $180 million has been allocated to a range of projects around the country that focus on producing green hydrogen and demonstrating how it can be used safely in a blend of natural gas.

A national blending target will build renewable hydrogen production capacity and gain consumer acceptance of a cleaner gas alternative for use in the home for cooking, heating and providing hot water. It will also build a domestic hydrogen market to support a viable export industry.

Figure 4: Decarbonisation pathways (Source: Gas Vision 2050)

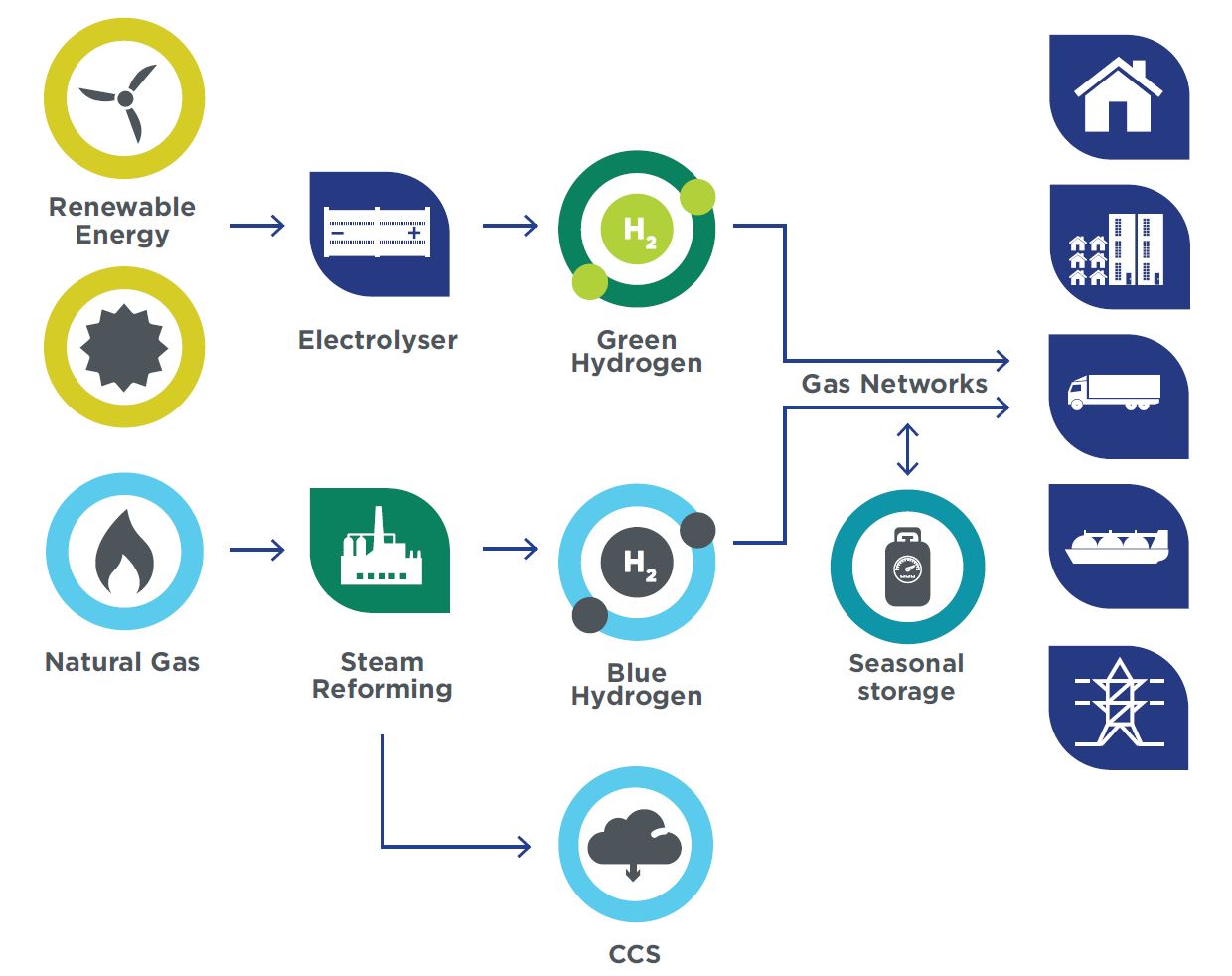

Hydrogen is already produced at commercial scale from natural gas, but this clearly means that it is currently more expensive than the gas used to make it. This process also generates carbon dioxide, which would need to be removed using carbon capture and storage in a net-zero world.

An alternative technology is to apply an electric current to water, which produces hydrogen gas. When this uses renewable electricity, it provides a net-zero emissions fuel.

Both options are more costly than natural gas today, but with continued investments, the costs will fall in the next few years to become cost-competitive.

Solar PV went through a similar journey only a few years ago, with it being uncompetitive for power generation in the early 2000s to now being one of the lowest-cost generation technologies[i].

Figure 5: Hydrogen production pathways and usage (Source: Gas Vision 2050)

Gas provides heating services to many homes and businesses and is an essential feedstock for industry. It supports many hundreds of thousands of direct and indirect jobs and delivers enormous economic benefits to the nation.

There are activist groups calling for gas to be turned off, and all the services it provides to be electrified. To support the case, these groups tend to rely on simplified calculations with generous assumptions about the performance of electrical appliances and their ability to provide the equivalent (to gas) quality and amount of heat. They also ignore the amenity value of gas (think a decorative gas fireplace on a cold winter’s night) and its value in giving customers a choice.

Electrification advocates also commonly ignore the whole-of-system costs when making claims about how much money can be saved from switching to electric heat pumps.

During the update of Gas Vision 2050, we completed a range of scenarios to consider the value of gaseous fuels and the gas infrastructure in achieving net-zero emissions from the energy sector[ii].

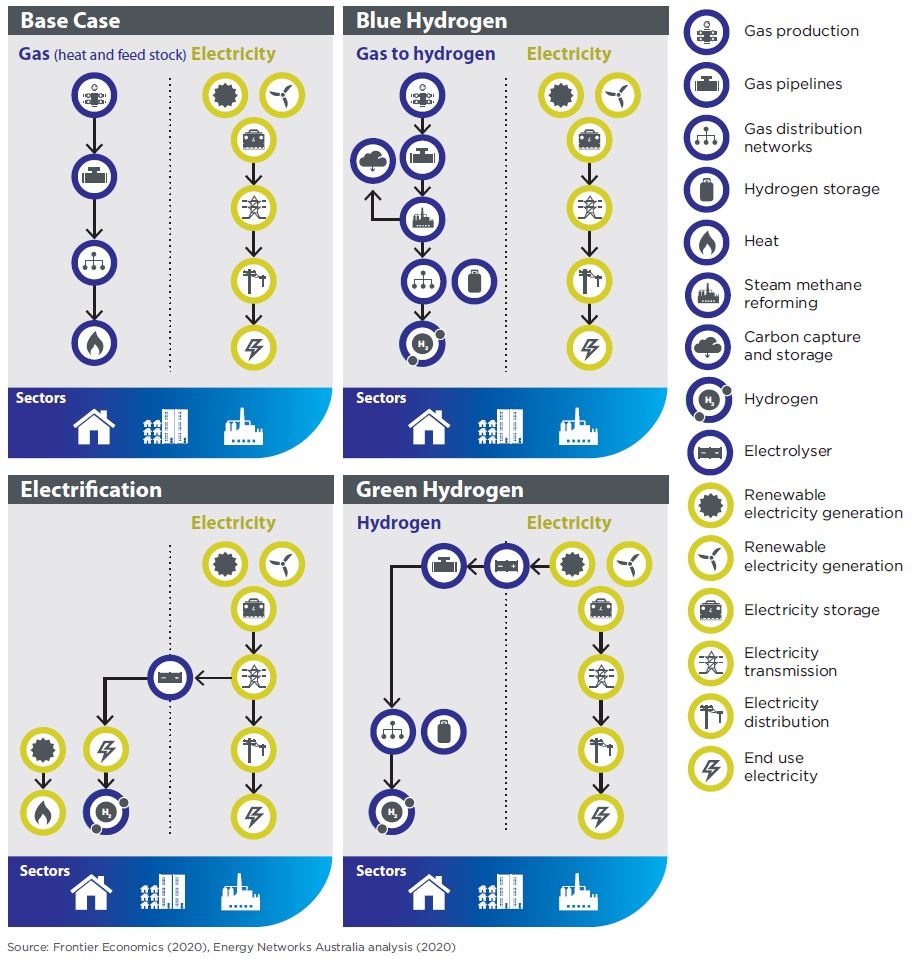

These scenarios assumed that the electricity sector would reach net-zero emissions by 2050 and that the gas sector would reach zero emissions via one of the three options:

- Blue hydrogen: where natural gas is produced and provided to steam methane reforming to produce hydrogen, which is injected into the gas distribution network, while the resulting CO2 is removed with CCS.

- Green hydrogen: where hydrogen is produced from renewable electricity generation in the renewable energy zones[iii] and then transported to the end consumer via new hydrogen ready pipelines and the existing distribution network.

- Electrification: where all gas infrastructure is decommissioned, and the energy provided by gas is provided through additional electricity generation and networks.

Figure 6: Net-zero pathways (Source: Gas Vision 2050)

In all cases, the ongoing annual cost was estimated compared with the base case, where only the electricity sector reached net-zero. This provided us with a clear understanding of the ongoing costs of different technology options to reach the same net-zero emissions outcome by 2050.

The main finding is that net-zero emissions can be achieved with hydrogen at roughly half the cost of electrification.

Gas distribution networks are constructed of plastic materials that are compatible with delivering hydrogen as a fuel in place of natural gas. Gas pipelines could be repurposed or rebuilt to carry hydrogen at a much lower cost than delivering the equivalent energy through electricity transmission lines.

Furthermore, gas infrastructure also chemical feedstock to industrial processes which cannot be electrified.

There is a clear benefit to being able to continue providing energy with gas pipelines and gas networks.

Policy settings aimed at reducing emissions should be technology-neutral and recognise that continuing to use gas infrastructure is the lowest cost option to reach net-zero emissions from the energy sector by 2050. This will be far cheaper for customers compared with electrification.

Continued support aimed at removing commercial and regulatory risk for hydrogen and to accelerate its cost competitiveness will provide better and cheaper options for a future decarbonised energy sector.

References

[i] Even though solar PV is often claimed to be one of the lowest cost of generation, it still remains an intermittent source.

[ii] In the modelling, both the electricity and the gas consumption sectors were modelled to reach net-zero by 2050.

[iii] These are the Renewable Energy Zones as identified in AEMO’s Integrated Systems Plan