Hydrogen’s aim better with a target?

The Paris Climate Change Agreement, agreed in 2015 and ratified the following year, has been instrumental in focussing global attention to reduce greenhouse gas emissions.

Simply, the agreement aims for countries to reach peak emissions as soon as possible and to reach net-zero emissions in the second half of the century to limit global warming to two degrees[i].

Many countries have responded to this by setting national targets of net-zero emissions by 2050.

Australia has ratified the Paris agreement, and while the nation has not set an emissions target for 2050, all states and territories have set net-zero emissions by 2050 targets.

The ACT is even more ambitious, bringing this forward to 2045.

So in effect, all onshore activities are covered by a net-zero target.

Given all this, do we need a target for hydrogen to get the market moving faster?

Targets at work

Developing new industries can benefit from setting targets.

These targets can be narrow or broad, technology or market focussed, local or national, but they are important to focus activity. Quite often, there are a range of targets and incentives, working together to achieve the desired outcomes.

The Renewable Energy Target (RET) shows that setting targets work. The RET is a legislated requirement on electricity retailers to source a given proportion of specified electricity sales from renewable generation sources. It intended to grow the renewable generation market to make lower carbon cost electricity generation technologies more commercially competitive. Its intention was not to directly reduce greenhouse gas emissions.

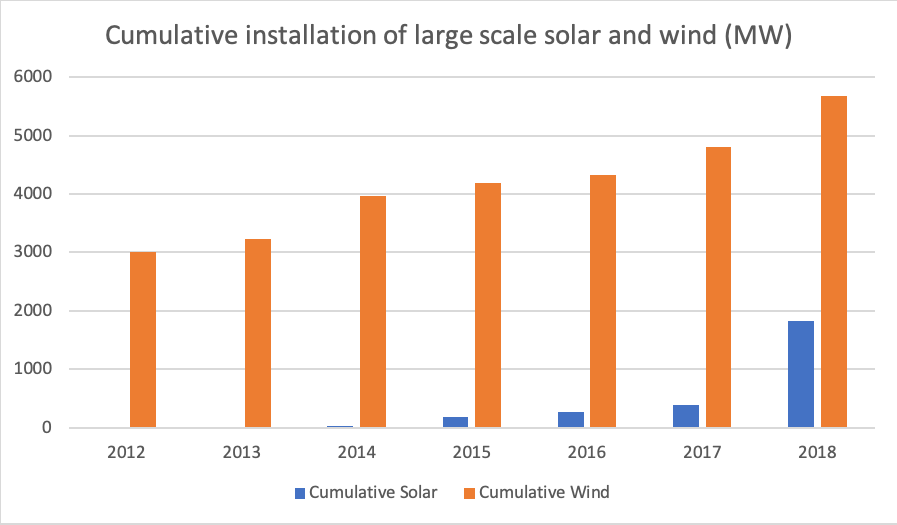

In the early stages of the RET, most of the projects were focussed on wind, so subsequent incentives were introduced by ARENA through its Large Scale Solar round to drive down the cost of utility-scale solar. This shift has helped, as shown by the data collected by the Clean Energy Council.[ii]

Figure 1: The impact of targeted policy support for large scale solar.[iii]

At the household scale, state-based feed-in tariffs and additional government grants also supported the increase of rooftop PV.

The rates of installation were also driven by cost reductions in solar PV systems – due to a combination of cost reductions from global manufacturing and supply chains of solar PV panels[iv] and installation costs reductions from local experience.

So it was not the RET by itself that established renewable energy as a cost-competitive option, but rather several policies and incentives working together and supported by global technology developments.

Hydrogen targets

Hydrogen can similarly benefit from targets and incentives.

At a global level, several targets are being set. For example[v]:

- The Japanese Government has set a target to procure 300,000 tonnes of low-emissions hydrogen annually by 2030;

- South Korea is aiming to produce 6.2 million hydrogen fuel cell vehicles for domestic use and export, as well as build 1,200 refuelling stations by 2040.

These targets are mostly driven by national decarbonisation targets and recognise the role of hydrogen to help achieve that.

Australia has a few different and complementary targets for hydrogen.

- The Commonwealth Government has set a technology target of producing a kilogram of hydrogen for under $2 (equivalent to $16.67/GJ). The Government recognises that at this price point, hydrogen will become a commercially competitive option for many applications, including exports.

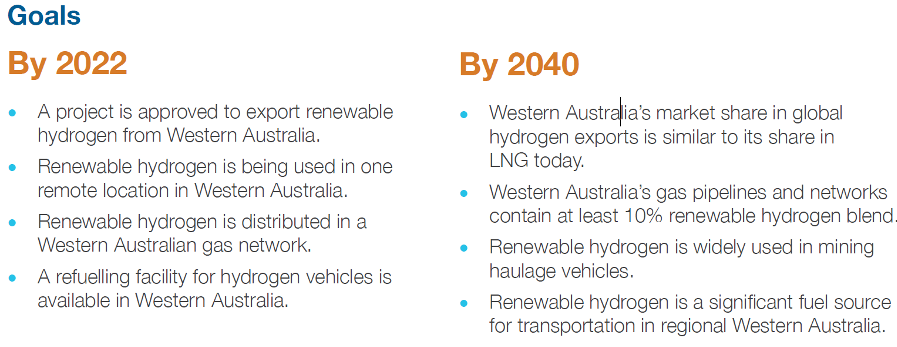

- In its Western Australian Renewable Hydrogen Strategyiii, WA has set aspirational targets covering a broad range of hydrogen opportunities.

Figure 2: Western Australian clean hydrogen targets.[vi]

- Similarly, the NSW Government released its plan[vii] earlier this month. It indicated it would establish a dedicated hydrogen program to help scale up hydrogen as an energy source and feedstock. The NSW Government also indicated it would set up an aspirational target of 10 per cent hydrogen in the gas network by 2030.

Sorting out the targets

It is easy to become confused about whether these targets work together or if they are counterproductive.

Each of the targets plays different roles, but all aim at achieving the same objective of net-zero emissions.

The combination of hydrogen targets is not dissimilar to what happened in the early days of the RET. As noted above, additional incentives and targets were needed to achieve the levels of renewable generation now in the market.

A significant difference is that the renewable electricity targets were supported (and continue to be supported) by a range of financial incentives which drove the uptake of that technology, and hence its cost reduction. Similarly, incentives for hydrogen production could accelerate the take up of hydrogen as a fuel source, bring down the cost and accelerate commercial maturity of clean hydrogen.

All the mechanisms that have been used for renewable electricity could easily be modified to support the development of a renewable gas production industry.

Time will tell whether this proven model will be adopted to facilitate hydrogen deployment at scale.

References

[i] Greater aspirations to limit warming to 1.5 degrees were included as a possible future consideration in the Paris Agreement.

[ii] https://assets.cleanenergycouncil.org.au/documents/resources/reports/clean-energy-australia/clean-energy-australia-report-2019.pdf

[iii] https://assets.cleanenergycouncil.org.au/documents/resources/reports/clean-energy-australia/clean-energy-australia-report-2019.pdf

[iv] Increased global demand was driven by similar renewable energy target set by many countries around the world.

[v] WA Department of Primary Industries and Regional Development (2019), Western Australian Renewable Hydrogen Strategy.

[vi] WA Department of Primary Industries and Regional Development (2019), Western Australian Renewable Hydrogen Strategy

[vii] NSW Department of Planning, Inudstry and Environment (2020), Net Zero Plan Stage 1: 2020-2030