Out of the mire…getting carbon policy back on track

The release of the Climate Change Authority’s (CCA) climate policy toolkit[1] and research report[2] resulted in fierce, renewed debate over the last week about appropriate carbon targets and policy settings.

The CCA report was criticised in some quarters for not assessing the adequacy of the current Australian Government target, prompting a minority report from its own dissenting board members.[3] The debate has largely focused on the scale of the target rather than the policy options proposed.

The response to the report highlighted the acrimony that has mired Australian carbon policy. It highlighted the need for an institutional framework that not only enables the achievement of current targets, but is adaptive to expanded abatement objectives under the ‘ratchet’ mechanism envisaged by COP 21 in Paris.

The forthcoming 2017 review of Australia’s carbon policy framework, including the ERF Safeguards Mechanism is clearly the opportunity to end the ‘Mexican stand-off’ frustrating efficient abatement outcomes. No one argues that Australia’s existing carbon abatement target of 26 to 28% below 2005 levels by 2030 can or should be funded from the Federal Budget under an expanded Emission Reduction Fund. Australia must pursue an enduring, stable and nationally-integrated carbon policy framework based on consensus, and it needs to start now.

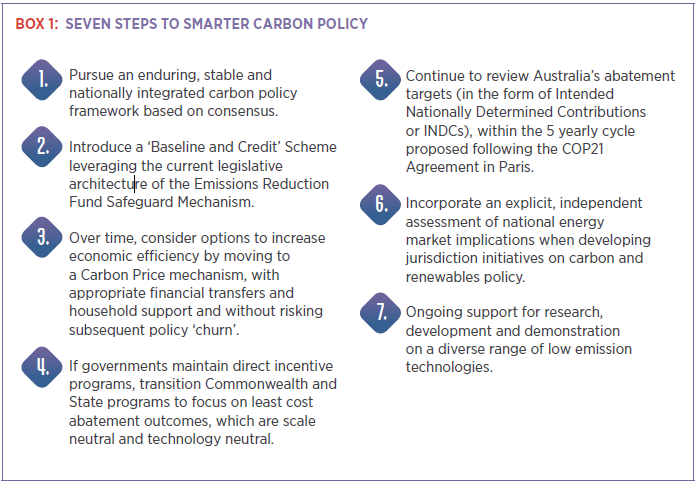

Prior to the release of the CCA report, the Energy Networks Association (ENA) released its carbon policy options paper, Enabling Australia’s Cleaner Energy Transition[4], which proposes Seven Steps to Smarter Carbon Policy (as detailed in Box 1 below) and is underpinned by detailed analysis by Jacobs.

Achieving abatement targets

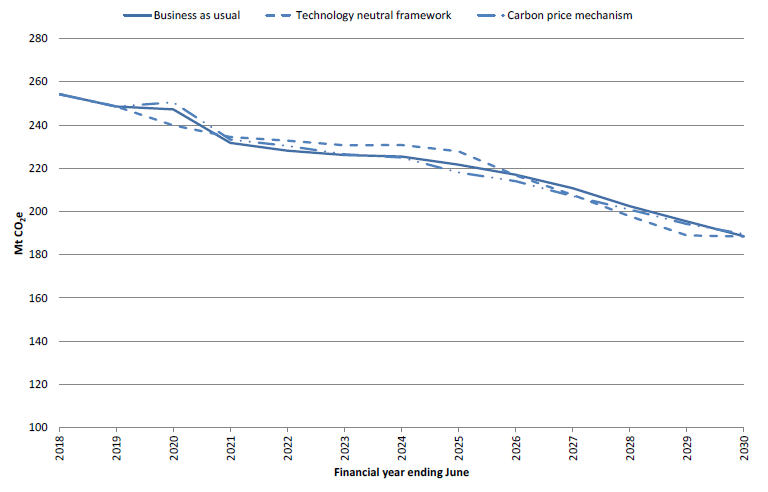

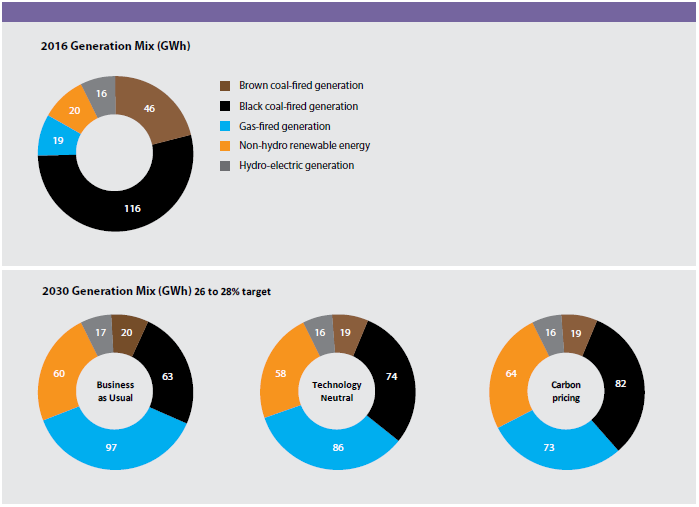

The Jacobs analysis for the ENA[5] evaluated three different policy settings for achieving the current Australian abatement target (26 to 28% below 2005 levels by 2030)[6]:

- Business as Usual – where the suite of current State and Federal government policies continues and major policy settings are adjusted to reach specific abatement targets.

- Technology Neutral – where the current suite of policies is adjusted to become technology neutral and elements of a ‘Baseline and Credit’ scheme are introduced.

- Carbon Price Mechanism – where all policies are removed and replaced by a carbon price on all emissions.

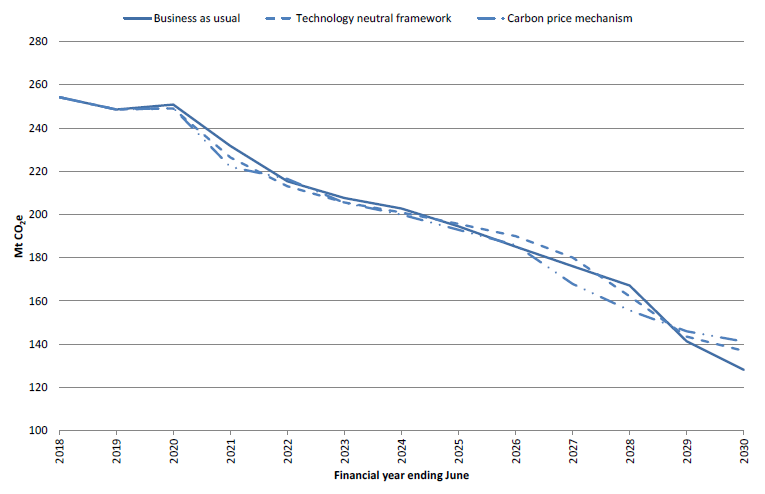

The results from the analysis demonstrate that the 2030 target could be met in any of the three scenarios. Jacobs also considered the option of a 45% target by 2030 for the ENA.

Modelling for the ENA and CCA shows that abatement targets can be met through a wide range of policy settings, with the main difference being in the total resource costs and the impact on residential bills.

ENA, 2016 – 26 to 28% target by 2030

ENA, 2016 – 45 % target by 2030

Impact on residential bills

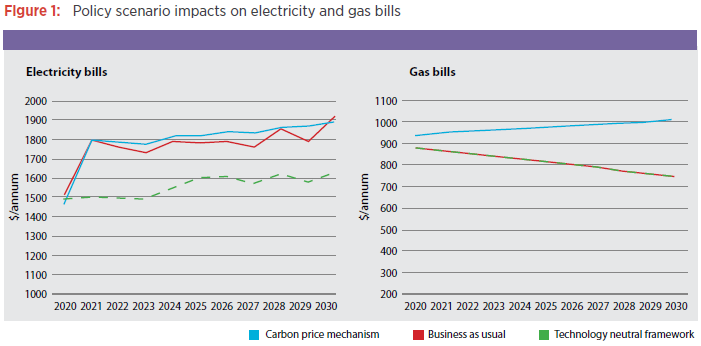

The introduction of a baseline and credit scheme for the electricity sector will allow abatement targets to be reached with lowest impact on the average household electricity bill, according to the Jacobs modelling for the ENA. The figure below presents the results of reaching a 26 to 28% target in 2030, and illustrates that the emissions intensive (technology neutral) scenario is able to reach the 2030 target at an average saving of $216 per annum over the decade. The modelling also showed that for a 45% abatement target in 2030, the technology neutral approach would provide savings of at least an average of $121 per year on household electricity bills compared to other scenarios (including ‘technology pull’ schemes).

The Climate Change Authority modelling assessed the residential tariff impacts of its scenarios and found too, that the lowest cost of carbon occurred by using market-based mechanisms, including either an emissions intensity scheme or a cap and trade scheme. As the CCA notes on page 46 of its report[7]:

…the market mechanisms are projected to have the lowest resource costs and costs per unit of emissions reductions (‘cost of abatement’) under the 2 degrees emissions budget…

The CCA modelling found that the emissions intensity scheme and cap and trade approaches resulted in a cost per tonne of CO2-e abated at less than $30 compared to technology pull mechanisms, one of which approached a cost of $40 per tonne of CO2-e abated.[8]

These consistent findings – for the different emissions abatement pathways in the different reports/modelling – demonstrate the value of market mechanisms in pursuing abatement targets. These market mechanisms also provide additional flexibility for increasing the abatement targets over time.

Renewable energy growth

Importantly, calls for technology neutral policy settings and market-based mechanisms are not an attack on renewables. Significant growth in renewable energy generation occurs in each of the modelling exercises.

In all scenarios modelled for the ENA, the Renewable Energy Target of 33,000 GWh is met by 2020. Renewable generation output grows to reach at least 74,000 GWh by 2030, as shown below.

Impact of policy mechanisms on NEM generation mix in 2030.

As Jacobs says for the CCA[9]:

In all the policy scenarios, renewable energy eventually becomes the dominant form of generation, with the proportion of renewable energy reflecting the impact of policy measures on generation costs and any restrictions limiting the type of technologies available. The level of renewable energy is highest in the technology pull scenarios due to policy directly providing a subsidy for those technologies. Renewable generation is lower in the emissions pricing scenarios, where gas plays a more significant role in the early years, and low emission technologies (such as CCS and nuclear) play a role later.

Both modelling exercises show significant ongoing growth in renewable energy investment under technology neutral frameworks. This underscores the increasing commercial maturity of these sources and their ability to compete on a level playing field to achieve efficient abatement.

If markets are allowed to work, each technology finds its efficient role and the power system is in a stronger position to support more renewable energy, while avoiding reliability and security risks for customers.

An increasing target

As noted above, the most intense debate has been focused on the size of the target, rather than on the pathway to achieving the target. Informed by science, Australia can ’ratchet up’ its target through the five-yearly reviews agreed at Paris. Energy Minister Josh Frydenberg has confirmed that the Paris commitment would have to be increased over time to keep global warming within 2 degrees[10]:

… there will have to continue to be changes in the targets and that’s why there are five-yearly reviews that were agreed at Paris and Australia was one of the proponents of those reviews taking place.

The economic analysis undertaken for both the ENA and CCA indicates the capacity to achieve current or increased targets. However, the efficiency with which those targets are achieved is highly dependent on not only the policy framework adopted, but its predictability and durability.

In the short-term, an emissions intensity baseline and credit scheme provides scope to get Australian carbon policy back on track.

If the support for such changes is both bipartisan and intergovernmental, Australia will be better placed to meet its international climate obligations in an efficient manner. If Australia can secure tangible progress with consensus today, it can review and tighten its carbon targets and refine emissions trading options over time.

The Jacobs analysis for the ENA and consultation on the proposed policy measures will inform development of the forthcoming Electricity Network Transformation Roadmap by the ENA and CSIRO. ENA is seeking feedback on the policy measures identified in Enabling Australia’s Cleaner Energy Transition by Friday 30 September 2016.

[1] Climate Change Authority (2016), Towards a Climate Policy Toolkit: Special Review on Australia’s Climate Goals and Policies, available from www.climatechangeauthority.gov.au

[2] Climate Change Authority (2016), Policy Options for Australia’s Electricity Supply Sector, available from www.climatechangeauthority.gov.au

[3] Climate Council, 5 September 2016, Climate Change Authority Special Review: Minority Report, https://www.climatecouncil.org.au/cca-minority-report

[4] Energy Networks Association (August, 2016) Enabling Australia’s Cleaner Energy Transition, available from www.ena.asn.au/publications

[5] Jacobs (22 August, 2016) Australia’s Climate Policy Options – Modelling of Alternate Policy Scenarios, available from www.ena.asn.au/publications

[6] The Jacobs report also assesses a higher target of 45% below 2005 levels by 2030.

[7] Climate Change Authority (2016), Policy Options for Australia’s Electricity Supply Sector, available from www.climatechangeauthority.gov.au

[8] See the Comparison Chart at page 47 of the CCA report and reproduced in a separate Energy Insider article in today’s edition.

[9] Jacobs (25 August, 2016) Modelling illustrative electricity sector emissions reduction policies (Climate Change Authority) Final report, http://climatechangeauthority.gov.au/sites/prod.climatechangeauthority.gov.au/files/files/SR%20Modelling%20reports/Jacobs%20modelling%20report%20-%20electricity.pdf