Money, Money, Money, it’s always sunny

The Energy Security Board’s recommendations for the energy market post-2025 have landed and the Australian Energy Market Operator (AEMO) is busily working on the Integrated System Plan (ISP) for 2022. Both market bodies are focussing on a National Energy Market (NEM) shaped future, with NEM-shaped approaches and results. Meanwhile, the states haven’t got that memo. They are vigourously pursuing their own state- based plans and approaches to deliver the clean energy future their constituents desire.

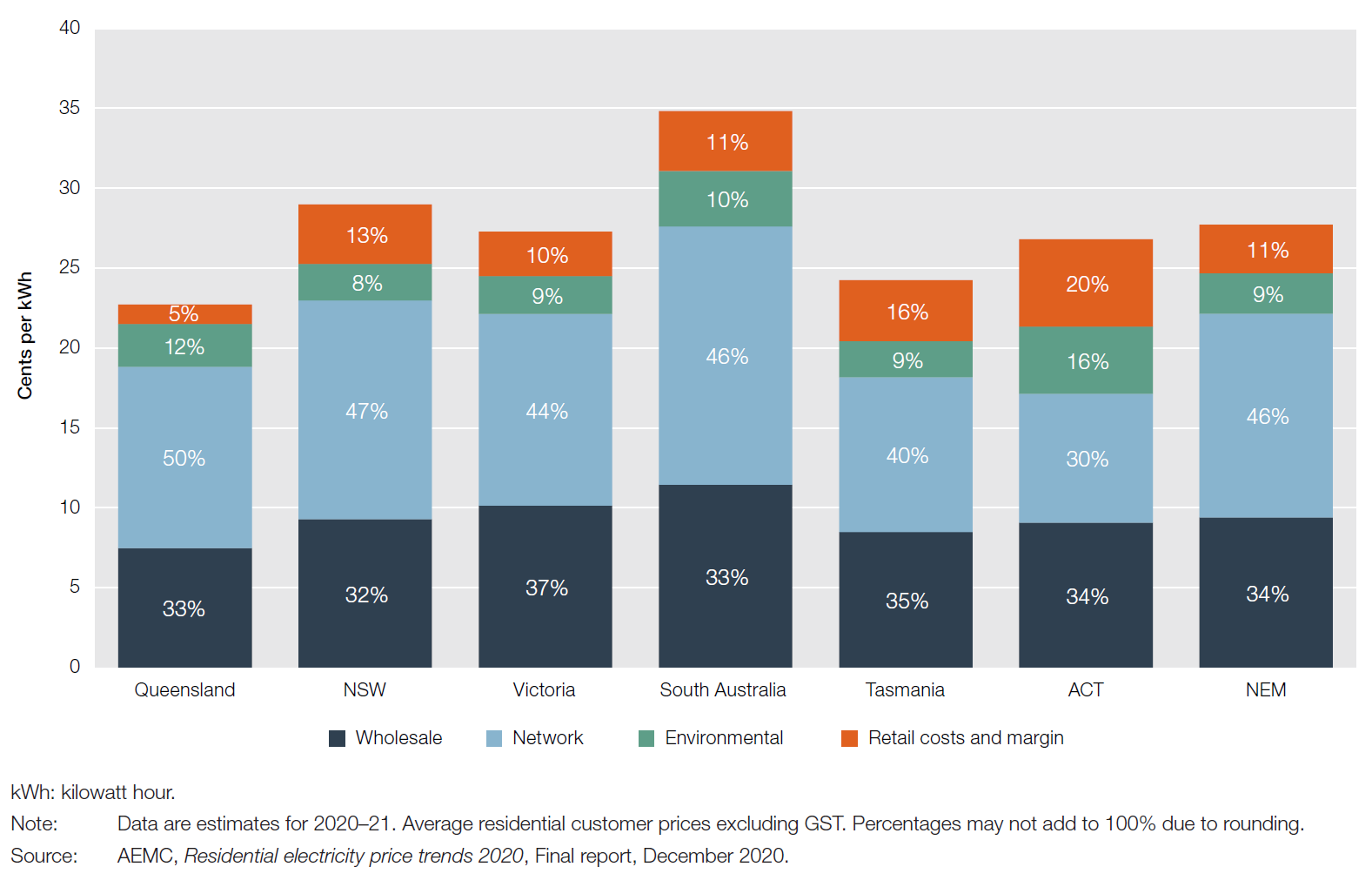

Centrally planned investment in network infrastructure outlined in the ISP is passed onto customers and is included in the bill from their retailer, though use of system charges at the transmission and distribution level – the price we pay to use the networks (pale blue in the diagram below). All generators recover their investment costs, via the price for their energy, again seen in the retail bill (dark blue). The costs retailers incur to run their business and look after customers is also in the bill (orange).

Figure 1: Breakdown of electricity bills

The incentives that drive the investment in renewable energy like solar PV and wind are also funded through our electricity bills (green). And the funds to support AEMO to undertake planning and operate the power system safely and securely are also provided through the bill (smeared over retailer, wholesale (generator) and network – with network only recently being added for transmission only). The electricity bill is already a very hardworking document[1].

Recently, federal and state funding has supported early works into some of the interconnectors, towers and wires that run between states, earmarked for construction in the earlier ISPs. This includes Project Energy Connect (NSW-SA) and Marinus Link (Tasmania-Victoria). This means some of the costs of these projects are carried by taxpayers and are not in the electricity bill.

With more than 2.3 million Australian households having rooftop solar PV, more of us are making and using our own electricity. This is perfect when the sun is shining overhead, but what happens when the sun isn’t shining locally? This is where renewable generation, large and small, in other locations is important, since it provides diversity in supply and ensures electricity can be imported from afar, when locally there is little or no generation.

For the state-based schemes, such as NSW’s and Victoria’s Renewable Energy Zones, the costs of connecting the new renewable generation to the wider grid, will be borne by customers, again via the electricity bill.

In NSW a more complex arrangement will see the costs of the renewable generation and transmission flow to customers via distribution network use of system charges (part of the pale blue percentage in Figure 1) through contracts for difference.

In the ACT, aspirations for clean electricity saw the state government strike agreements direct with renewable generators several years ago at a fixed long-term price. The costs of these agreements appear in ACT customers’ bills as distribution use of system charges (pale blue), rather than as the wholesale electricity price (dark blue). Wholesale electricity prices have now dropped below the agreed contract price and so Canberrans are paying 40 per cent higher network charges and bills as a result

There are other models, where the newly built and connecting generators fund the wires that link them to the grid such as the new Dedicated Connection Assets (DCA) option, but this is not the model proposed for NSW.

Care is needed to “smooth” what the customer sees, with the risk that the costs of new investment in networks and generation will land in customers’ bills well before the tangible benefits from lower electricity prices do.

Electricity bills represent 2.6-4.9 per cent of the average household spend, but energy bills represent a disproportionate amount of the disposable income of a vulnerable customer, some 3.9-8.5 per cent[2]. Vulnerable customers also typically have fewer options to manage their electricity use to reduce the costs, since they are often renting and are, for example, unable to invest in rooftop Solar PV [3].

The AEMO ISP provides a route to deliver new generation and transmission at least cost to consumers. Significant investment of $6-$12 billion is needed for transmission in the coming years to deliver net benefits of $11 billon[4]. It is difficult to see how a myriad of state-led approaches can deliver more cost-effectively than a NEM-led approach.

Money isn’t funny for many Australians and managing the transition to clean electricity in a way that is equitable and considers the balance between local generation versus distant generation will ensure that the benefits and costs are apportioned in a way to minimise the impact on consumers.

[1] https://www.aer.gov.au/system/files/State%20of%20the%20energy%20market%202021%20-%20Chapter%206%20-%20Retail%20energy%20markets.pdf

[2] https://www.aer.gov.au/system/files/Affordability%20in%20retail%20energy%20markets%20-%20September%202019_0.pdf

[3] https://www.acoss.org.au/wp-content/uploads/2017/07/ACOSS_BSL_TCI_Empowering-households.pdf

[4] https://aemo.com.au/-/media/files/major-publications/isp/2020/final-2020-integrated-system-plan.pdf?la=en&hash=6BCC72F9535B8E5715216F8ECDB4451C